- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 27-06-2017

(raw materials / closing price /% change)

Oil 43.72 -1.18%

Gold 1,247.50 +0.05%

(index / closing price / change items /% change)

Nikkei +71.74 20225.09 +0.36%

TOPIX +6.81 1619.02 +0.42%

Hang Seng -31.90 25839.99 -0.12%

CSI 300 +6.63 3674.72 +0.18%

Euro Stoxx 50 -23.44 3538.32 -0.66%

FTSE 100 -12.44 7434.36 -0.17%

DAX -99.81 12671.02 -0.78%

CAC 40 -37.17 5258.58 -0.70%

DJIA -98.89 21310.66 -0.46%

S&P 500 -19.69 2419.38 -0.81%

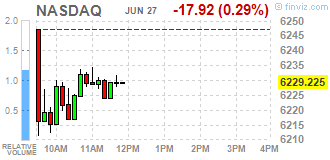

NASDAQ -100.53 6146.62 -1.61%

S&P/TSX -34.80 15281.22 -0.23%

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1335 +1,34%

GBP/USD $1,2812 +0,72%

USD/CHF Chf0,96 -1,23%

USD/JPY Y112,27 +0,37%

EUR/JPY Y127,26 +1,71%

GBP/JPY Y143,82 +1,08%

AUD/USD $0,7579 -0,03%

NZD/USD $0,7262 -0,29%

USD/CAD C$1,3194 -0,41%

06:00 United Kingdom Nationwide house price index, y/y June 2.1%

06:00 United Kingdom Nationwide house price index June -0.2%

06:00 Switzerland UBS Consumption Indicator May 1.48

06:45 France Consumer confidence June 102 103

08:00 Eurozone Private Loans, Y/Y May 2.4% 2.5%

08:00 Eurozone M3 money supply, adjusted y/y May 4.9% 5%

12:30 U.S. Goods Trade Balance, $ bln. May -67.55 -66.2

13:30 Eurozone ECB President Mario Draghi Speaks

13:30 United Kingdom BOE Gov Mark Carney Speaks

13:30 Canada BOC Gov Stephen Poloz Speaks

13:30 Japan BOJ Governor Haruhiko Kuroda Speaks

14:00 U.S. Pending Home Sales (MoM) May -1.3% 0.8%

14:30 U.S. Crude Oil Inventories June -2.451

23:50 Japan Retail sales, y/y May 3.2% 2.6%

The main US stock indices fell noticeably. Pressure on the market provided sales in the technological segment and conglomerate sector, while some support was provided by the market from the growth of shares of banks, as well as securities of the energy sector.

In addition, investors reacted to the message that the confidence of consumers unexpectedly improved. The Conference Board said that the consumer confidence index rose to 118.9 in June. It was expected to decline to 116 from 117.6 in May. The index of the current situation increased by 5.3 points to 146.3, while the index of expectations fell by 1.7, to 100.6. At the same time, the S & P / Case-Shiller report showed that prices for single-family homes in the US accelerated at a slower pace than expected in April. According to the report, the composite index for 20 megacities rose in April at 5.7% per annum after an increase of 5.9% in March. The growth was forecasted at 5.9%.

Attention of market participants was also attracted by reports that the IMF worsened the outlook for the US economy due to doubts about the effectiveness of measures promised by Tramp to reduce taxes and increase spending on infrastructure. The IMF expects US GDP growth by 2.1% in 2018 against the previous forecast of + 2.5%, and predicts a slowdown in growth to 1.7% in the next 5 years. The IMF also believes that the US dollar rate is 10% -20% higher than the level justified in terms of economic fundamentals. In addition, the IMF said that the Fed should continue to raise interest rates "depending on the incoming data."

Most components of the DOW index finished trading in the red (22 of 30). Most fell shares of Verizon Communications Inc. (VZ, -1.76%). Leader of the growth were JPMorgan Chase & Co. shares. (JPM, + 1.18%).

Most sectors of the S & P index showed a decline. The conglomerate sector fell most of all (-2.0%). The leader of growth was the financial sector (+ 0.3%).

At closing:

DJIA -0.45% 21.313.54 -96.01

Nasdaq -1.61% 6,146.62 -100.53

S & P -0.80% 2.419.45 -19.62

Major U.S. stock-indexes were little changed, as equities managed to retrace a good portion of their opening losses. The investors' sentiment remained subdued due to continuing selloff in technology shares and ahead of the speech by Federal Reserve Chair Janet Yellen. On the contrary, names, belonging to financial and energy sectors, helped to keep the broader market afloat. Better-than-expected consumer confidence data also provided some support to the market.

A majority of Dow stocks in negative area (16 of 30). Top loser - Verizon Communications Inc. (VZ, -1.84%). Top gainer - JPMorgan Chase & Co. (JPM, +1.50%).

Most of S&P sectors in negative area.Top loser - Utilities (-0.7%). Top gainer - Basic Materials (+0.8%).

At the moment:

Dow 21381.00 +13.00 +0.06%

S&P 500 2436.75 +0.75 +0.03%

Nasdaq 100 5763.00 -15.25 -0.26%

Crude Oil 44.41 +1.03 +2.37%

Gold 1247.80 +1.40 +0.11%

U.S. 10yr 2.20 +0.06

The Conference Board Consumer Confidence Index, which had decreased in May, increased moderately in June. The Index now stands at 118.9 (1985=100), up from 117.6 in May. The Present Situation Index increased from 140.6 to 146.3, while the Expectations Index declined from 102.3 last month to 100.6.

"Consumer confidence increased moderately in June following a small decline in May," said Lynn Franco, Director of Economic Indicators at The Conference Board. "Consumers' assessment of current conditions improved to a nearly 16-year high (July 2001, 151.3). Expectations for the short-term have eased somewhat, but are still upbeat. Overall, consumers anticipate the economy will continue expanding in the months ahead, but they do not foresee the pace of growth accelerating."

EURUSD: 1.1150 (EUR 210m) 1.1200 (560m) 1.1230 (340m) 1.1300 (470m) 1..1350 (610m)

USDJPY: 111.00 (USD 400m) 111.50 (420m) 111.80 (270m) 112.00-10 (685m) 113.00 (200m)

GBPUSD: 1.2625 (GBP 285m) 1.2725 (228m) 1.2740 (265m)

EURGBP: 0.8700 (EUR 320m) 0.8820 (554m) 0.8940 (265m)

AUDUSD: 0.7600-06 (AUD 533m)

USDCAD: 1.3175 (USD (200m) 1.3250-60 (610m) 1.3330 (260m) 1.3365 (265m)

EURJPY: 124.75 (EUR 185m)

U.S. stock-index futures slipped, as a selloff in technology shares continued, while investors awaited the speech by Federal Reserve Chair Janet Yellen.

Stocks:

Nikkei 20,225.09 +71.74 +0.36%

Hang Seng 25,839.99 -31.90 -0.12%

Shanghai 3,191.51 +6.07 +0.19%

S&P/ASX 5,714.19 -5.97 -0.10%

FTSE 7,433.86 -12.94 -0.17%

CAC 5,259.10 -36.65 -0.69%

DAX 12,689.72 -81.11 -0.64%

Crude $43.98 (+1.38%)

Gold $1,249.80 (+0.27%)

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 31.45 | 0.27(0.87%) | 11474 |

| Amazon.com Inc., NASDAQ | AMZN | 989.3 | -4.68(-0.47%) | 25566 |

| Apple Inc. | AAPL | 145.23 | -0.59(-0.40%) | 109456 |

| AT&T Inc | T | 37.94 | -0.21(-0.55%) | 51686 |

| Barrick Gold Corporation, NYSE | ABX | 16.49 | 0.15(0.92%) | 16061 |

| Boeing Co | BA | 200 | 0.02(0.01%) | 592 |

| Caterpillar Inc | CAT | 104.2 | -0.05(-0.05%) | 300 |

| Cisco Systems Inc | CSCO | 32.2 | -0.04(-0.12%) | 1681 |

| Citigroup Inc., NYSE | C | 64.01 | 0.23(0.36%) | 6098 |

| Exxon Mobil Corp | XOM | 81.27 | 0.03(0.04%) | 1423 |

| Facebook, Inc. | FB | 153 | -0.59(-0.38%) | 45356 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 11.91 | 0.09(0.76%) | 5237 |

| General Electric Co | GE | 27.66 | 0.05(0.18%) | 6701 |

| General Motors Company, NYSE | GM | 34.34 | -0.18(-0.52%) | 5618 |

| Goldman Sachs | GS | 221.8 | 1.36(0.62%) | 3113 |

| Google Inc. | GOOG | 940.01 | -12.26(-1.29%) | 18761 |

| Hewlett-Packard Co. | HPQ | 18.17 | 0.01(0.06%) | 100 |

| Intel Corp | INTC | 34 | -0.07(-0.21%) | 43267 |

| Johnson & Johnson | JNJ | 136.88 | 0.54(0.40%) | 734 |

| JPMorgan Chase and Co | JPM | 87.6 | 0.36(0.41%) | 4898 |

| Merck & Co Inc | MRK | 66.5 | 0.58(0.88%) | 231683 |

| Microsoft Corp | MSFT | 70.16 | -0.37(-0.52%) | 9559 |

| Nike | NKE | 53.2 | -0.08(-0.15%) | 1615 |

| Procter & Gamble Co | PG | 89.28 | -0.08(-0.09%) | 701 |

| Starbucks Corporation, NASDAQ | SBUX | 59.59 | -0.05(-0.08%) | 622 |

| Tesla Motors, Inc., NASDAQ | TSLA | 374.41 | -3.08(-0.82%) | 51387 |

| The Coca-Cola Co | KO | 45.42 | -0.01(-0.02%) | 2296 |

| Twitter, Inc., NYSE | TWTR | 18.34 | 0.05(0.27%) | 37148 |

| Verizon Communications Inc | VZ | 45.23 | -0.52(-1.14%) | 89196 |

| Yandex N.V., NASDAQ | YNDX | 27.26 | 0.09(0.33%) | 910 |

-

We will increase german research spending from 3 to 3.5 pct of gdp to stay at innovation forefront

-

We need to make sure the state remains effective without consuming a greater share of gdp

-

If we don't create stability in africa europe will face challenges that dwarf those of 2015 migration crisis

-

We mustn't let people drown in the mediterranean; need to work with turkey to tackle problem at source

EUR/USD

Offers: 1.1200 1.1220-25 1.1235 1.1250 1.1280 1.1300

Bids: 1.1180 1.1150 1.1130 1.1100 1.1080 1.1050

GBP/USD

Offers: 1.2745 1.2760 1.2780 1.2800 1.2830 1.2850

Bids: 1.2700 1.2680 1.2665 1.2650 1.2630 1.2600

EUR/JPY

Offers: 125.50 125.80 126.00 126.30 126.50 127.00

Bids: 125.00 124.80 124.50 124.20 124.00

EUR/GBP

Offers: 0.8800 0.8820 0.8835 0.8850-55

Bids: 0.8770 0.8750-55 0.87200.8700 0.8685 0.8650

USD/JPY

Offers: 112.00 112.20 112.35 112.50 112.80 113.00

Bids: 111.75-80 111.50 111.20 111.00 110.80 110.50

AUD/USD

Offers: 0.7600 0.7620 0.7635 0.7650

Bids: 0.7550 0.7520 0.7500 0.7480 0.7450

-

UK will require a level of resilience at least as great as currently planned and exceeds international minimum standards

-

Intense competition means risk margins have fallen, risk assessments declined

The survey of 115 firms, of which 59 were retailers, showed that the volume of sales and orders placed upon suppliers grew modestly - exceeding expectations in both cases - in the year to June. Overall, sales for the time of year were considered to be broadly in line with seasonal norms.

Looking ahead, however, growth in volumes of sales is expected to stall in the year to July, while orders are also expected to be flat.

Within the retail sector, grocers and non-store sectors performed particularly strongly. Internet sales volumes also picked in the year to June, with growth broadly in line with the long-run average, but retailers expect somewhat slower growth in the year to July.

-

Risks from domestic financial environment are at standard level

-

Expects to raise ccyb to 1.0 pct from 0.5 pct in november, with further one-year implementation phase

-

Uk consumer credit has grown rapidly, lenders may be placing undue weight on recent benign conditions

-

Fpc stands ready to cut ccyb rate if risks materialise that could tighten lending conditions

-

UK authorities to issue new recommendations on consumer credit in july, boe will bring forward consumer credit stress tests

-

Plans to raise banks' minimum leverage ratio requirement to 3.25 pct of exposures ex central bank reserves from 3 pct

-

Will continue to oversee brexit contingency planning by financial institutions, including for 'no deal' outcome

-

Expects to keep existing mortgage loan-to-income restrictions for long-term, tweaks benchmark for mortgage affordabilty test

-

We see growth above trend and well distributed across the euro area, but inflation dynamics remain more muted than one would expect

-

Factors that are weighing on the path of inflation, at present are mainly temporary factors that typically the central bank can look through

-

Ecb efforts slowed by a combination of external price shocks, more slack in the labour market and a changing relationship between slack and inflation

-

We will need to be gradual when adjusting our policy parameters

With regard to the consumer survey, the confidence climate index increased in June 2017 from 105.4 to 106.4. All components improved: economic, personal, current and future (from 122.0 to 123.6, from 100.2 to 100.9, from 105.2 to 105.7 and from 106.6 to 107.7, respectively). The balance concerning expectations on unemployment grew from 32.9 to 35.4. The balance on inflation perceptions referring to the last 12 months increased from -11.1 to -3.3 and the balance on inflation expectations for next 12 months grew from -14.1 to -3.7.

With reference to the business surveys, the composite business confidence climate index (IESI, Istat Economic Sentiment Indicator) increased from 106.2 to 106.4.

The confidence index in manufacturing increased from 106.9 to 107.3. Assessments on order books improved, while production expectations worsened. The balance on inventories decreased.

The confidence index in construction increases (index from 128.1 to 129.8). Assessments on order books/construction plans improved (from -26.7 to -23.4 the balance) and employment expectations worsened (balance from -4.1 to -5.1).

EUR/USD

Resistance levels (open interest**, contracts)

$1.1285 (2791)

$1.1261 (1880)

$1.1239 (966)

Price at time of writing this review: $1.1196

Support levels (open interest**, contracts):

$1.1171 (3680)

$1.1135 (4677)

$1.1093 (4391)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date July, 7 is 68091 contracts (according to data from June, 26) with the maximum number of contracts with strike price $1,1150 (4677);

GBP/USD

Resistance levels (open interest**, contracts)

$1.2919 (2220)

$1.2846 (2424)

$1.2799 (1054)

Price at time of writing this review: $1.2734

Support levels (open interest**, contracts):

$1.2655 (2770)

$1.2580 (1371)

$1.2492 (1668)

Comments:

- Overall open interest on the CALL options with the expiration date July, 7 is 32653 contracts, with the maximum number of contracts with strike price $1,2800 (2424);

- Overall open interest on the PUT options with the expiration date July, 7 is 29515 contracts, with the maximum number of contracts with strike price $1,2800 (2790);

- The ratio of PUT/CALL was 0.90 versus 0.89 from the previous trading day according to data from June, 26

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

-

Trump very pleased with developments on healthcare bill, continues to support ways to make it stronger

For May 2017 compared with May 2016:

-

Goods exports rose $395 million (8.7 percent) to 5.0 billion.

-

Milk powder, butter, and cheese rose $342 million (42 percent).

-

Meat and edible offal rose $30 million (4.5 percent)

-

Goods exports to China rose $140 million (17 percent).

-

Goods exports to Japan rose $96 million (34 percent).

-

Goods imports rose $635 million (15 percent) to $4.8 billion.

-

Intermediate goods rose $435 million (26 percent).

-

Consumption goods rose $65 million (5.8 percent).

-

Capital goods fell $22 million (2.3 percent).

-

Passenger motor cars rose $87 million (23 percent).

-

Petrol and avgas rose $62 million (91 percent).

-

Goods imports from Australia rose $118 million (24 percent).

-

Goods imports from China rose $101 million (13 percent).

The monthly trade balance was a surplus of $103 million (2.1 percent of exports).

The annual trade deficit widened to $3.8 billion, from $3.6 billion in April 2017.

European stocks finished with gains on Monday, helped by Italian banks after that country's government stepped in to shut down two failed lenders, and as Nestlé SA rallied after a hedge fund snapped up a big stake in the consumer-products giant.

The Dow industrials on Monday ended a string of daily losses at four, but the Nasdaq Composite faltered, putting pressure on the broader market. For the first half of 2017, the benchmark S&P 500 is on track to advance about 9%, with some analysts suggesting that the second half will likely be positive as well.

Global shares were higher in Asia-Pacific trade Tuesday, lifted in part by a stronger U.S. dollar, though markets in Australia bucked the trend due to declines in utility and mining stocks. Spot gold prices were recently down 0.2%, extending losses after Monday's flash crash, which was caused by suspected human error. It plunged 1% shortly after the opening call in London on Monday and traded about 1.8 million troy ounces in a minute, "which is more than the volumes traded seen during recent global risk events," noted ANZ Research.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers