- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 19-07-2017

(raw materials / closing price /% change)

Oil 47.09 -0.06%

Gold 1,240.90 -0.09%

(index / closing price / change items /% change)

Nikkei +20.95 20020.86 +0.10%

TOPIX +1.39 1621.87 +0.09%

Hang Seng +147.22 26672.16 +0.56%

CSI 300 +62.57 3729.75 +1.71%

Euro Stoxx 50 +21.60 3500.28 +0.62%

FTSE 100 +40.69 7430.91 +0.55%

DAX +21.66 12452.05 +0.17%

CAC 40 +42.80 5216.07 +0.83%

DJIA +66.02 21640.75 +0.31%

S&P 500 +13.22 2473.83 +0.54%

NASDAQ +40.74 6385.04 +0.64%

S&P/TSX +95.14 15244.71 +0.63%

(pare/closed(GMT +2)/change, %)

EUR/USD $1,1516 -0,32%

GBP/USD $1,3021 -0,10%

USD/CHF Chf0,95502 +0,07%

USD/JPY Y111,87 -0,15%

EUR/JPY Y128,85 -0,47%

GBP/JPY Y145,687 -0,29%

AUD/USD $0,7951 +0,49%

NZD/USD $0,7355 +0,16%

USD/CAD C$1,26006 -0,20%

01:30 Australia Changing the number of employed June 42.0 15

01:30 Australia Unemployment rate June 5.5% 5.6%

03:00 Japan BoJ Interest Rate Decision -0.1% -0.1%

03:00 Japan BoJ Monetary Policy Statement

04:30 Japan All Industry Activity Index, m/m May 2.1%

05:00 Japan BOJ Outlook Report

06:00 Germany Producer Price Index (YoY) June 2.8% 2.3%

06:00 Germany Producer Price Index (MoM) June -0.2% -0.1%

06:00 Switzerland Trade Balance June 3.4 2.89

06:30 Japan BOJ Press Conference

08:00 Eurozone Current account, unadjusted, bln May 21.5

08:30 United Kingdom Retail Sales (YoY) June 0.9% 2.6%

08:30 United Kingdom Retail Sales (MoM) June -1.2% 0.4%

11:45 Eurozone Deposit Facilty Rate -0.4% -0.4%

11:45 Eurozone ECB Interest Rate Decision 0% 0%

12:30 Eurozone ECB Press Conference

12:30 U.S. Continuing Jobless Claims 1945 1950

12:30 U.S. Philadelphia Fed Manufacturing Survey July 27.6 24

12:30 U.S. Initial Jobless Claims 247 245

14:00 Eurozone Consumer Confidence (Preliminary) July -1.3 -1.1

14:00 U.S. Leading Indicators June 0.3% 0.4%

22:45 New Zealand Visitor Arrivals June 8.0%

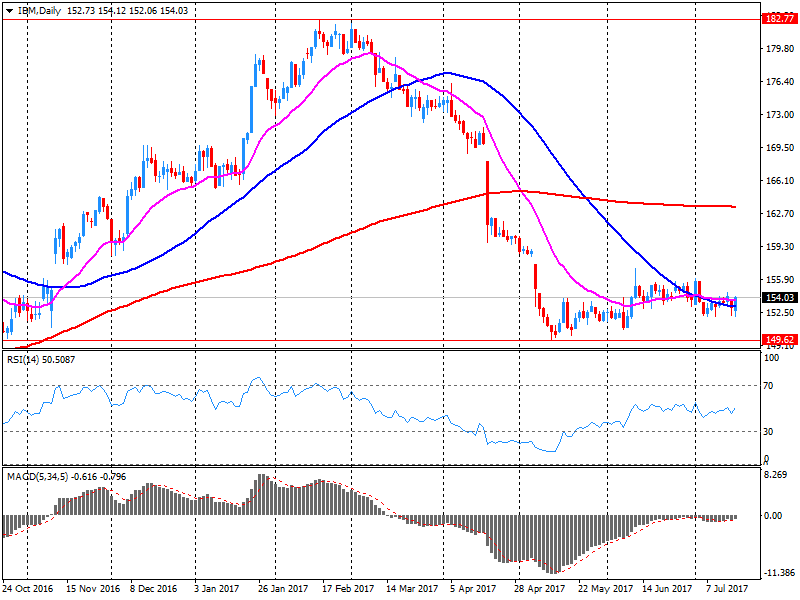

The main US stock indexes finished the auction with an increase, updating the record highs, which contributed to corporate reporting and statistics on the US housing market. At the same time, a significant decline in IBM shares prevented the Dow index from showing more serious growth.

According to the Ministry of Trade, housing construction finished the second quarter on a stronger note, as the bookings of new houses were restored in June at the fastest pace in four months. The laying of new homes increased by 8.3% to 1.22 million units (recalculated for annual rates). The laying of new houses for May was revised to 1.12 million from 1.09 million. Construction permits grew by 7.4% to 1.25 million per annum. The construction of single-family houses grew by 6.3% to 849,000 on an annualized basis. Bookmarks for apartment buildings jumped by 13.3% in June, to 366,000 in annual terms.

Oil prices rose by more than 1.5%, receiving support from statistics on oil products in the US, which indicated a more significant than expected decline in oil reserves. The US Energy Ministry reported that in the week of July 8-14, oil reserves fell by 4.727 million barrels to 490.62 million barrels. Analysts had expected a reduction of only 3.21 million barrels. Oil reserves in the Cushing terminal fell by 23 thousand barrels to 57.54 million barrels.

Most components of the DOW index recorded a rise (24 out of 30). The leader of growth was the shares of E. I. du Pont de Nemours and Company (DD, + 1.55%). Outsider were the shares of International Business Machines Corporation (IBM, -4.39%).

All sectors of the S & P index showed growth. The maximum increase was shown by the conglomerate sector (+ 1.2%).

At closing:

DJIA + 0.29% 21.636.50 +61.77

Nasdaq + 0.64% 6.385.04 +40.73

S & P + 0.53% 2.473.67 +13.06

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 4.7 million barrels from the previous week. At 490.6 million barrels, U.S. crude oil inventories are in the upper half of the average range for this time of year.

Total motor gasoline inventories decreased by 4.4 million barrels last week, but are in the upper half of the average range. Both finished gasoline inventories and blending components inventories decreased last week.

Distillate fuel inventories decreased by 2.1 million barrels last week but are near the upper limit of the average range for this time of year. Propane/propylene inventories increased by 3.5 million barrels last week but are in the lower half of the average range. Total commercial petroleum inventories decreased by 10.2 million barrels last week.

-

Says time to rebalance trade and investment relationship with China in fair, balanced manner

-

Must rebalance trade by selling more 'made in America' goods to China

EURUSD: 1.1300 (EUR 500m) 1.1400 (880m) 1.1450 (410m) 1.1475 (500m) 1.1500 (710m) 1.1600 (525m)

USDJPY: 110.30 (USD 500m) 112.25 (460m) 112.50 (440m)

GBPUSD: 1.2800 (GBP 375m)

EURGBP: 0.8764 (1.1bln)

EURJPY: 129.50 (EUR 690m) 130.00 (515m)

U.S. stock-index futures rose slightly as investors focused on Q2 earnings reports of the U.S. companies.

Global Stocks:

Nikkei 20,020.86 +20.95 +0.10%

Hang Seng 26,672.16 +147.22 +0.56%

Shanghai 3,232.87 +45.30 +1.42%

S&P/ASX 5,732.13 +44.73 +0.79%

FTSE 7,409.90 +19.68 +0.27%

CAC 5,190.43 +17.16 +0.33%

DAX 12,441.59 +11.20 +0.09%

Crude $46.45 (+0.11%)

Gold $1,240.80 (-0.09%)

(company / ticker / price / change ($/%) / volume)

| 3M Co | MMM | 210.99 | -0.69(-0.33%) | 320 |

| ALTRIA GROUP INC. | MO | 73.2 | -0.17(-0.23%) | 373 |

| Amazon.com Inc., NASDAQ | AMZN | 1,005.10 | -4.94(-0.49%) | 28093 |

| Apple Inc. | AAPL | 149.05 | -0.51(-0.34%) | 74367 |

| AT&T Inc | T | 36.4 | 0.01(0.03%) | 4115 |

| Barrick Gold Corporation, NYSE | ABX | 16.28 | 0.20(1.24%) | 13277 |

| Caterpillar Inc | CAT | 108.25 | 0.19(0.18%) | 865 |

| Chevron Corp | CVX | 104.8 | 0.59(0.57%) | 4041 |

| Cisco Systems Inc | CSCO | 31.53 | 0.03(0.10%) | 1525 |

| Citigroup Inc., NYSE | C | 66.48 | -0.35(-0.52%) | 15762 |

| Deere & Company, NYSE | DE | 125.91 | 0.03(0.02%) | 2583 |

| Exxon Mobil Corp | XOM | 81.1 | 0.24(0.30%) | 1080 |

| Facebook, Inc. | FB | 159.87 | 0.14(0.09%) | 58177 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 13.05 | 0.05(0.38%) | 18960 |

| General Electric Co | GE | 26.81 | -0.01(-0.04%) | 7450 |

| Goldman Sachs | GS | 226.55 | -2.71(-1.18%) | 115471 |

| Google Inc. | GOOG | 954.99 | 1.57(0.16%) | 1731 |

| Home Depot Inc | HD | 154.03 | 0.14(0.09%) | 295 |

| Intel Corp | INTC | 34.37 | -0.10(-0.29%) | 521 |

| International Business Machines Co... | IBM | 153.1 | 0.09(0.06%) | 2352 |

| Johnson & Johnson | JNJ | 132.92 | 0.77(0.58%) | 64420 |

| JPMorgan Chase and Co | JPM | 90.87 | -0.52(-0.57%) | 13932 |

| Microsoft Corp | MSFT | 73.4 | 0.05(0.07%) | 46429 |

| Procter & Gamble Co | PG | 87.57 | 0.02(0.02%) | 569 |

| Starbucks Corporation, NASDAQ | SBUX | 58.35 | 0.02(0.03%) | 1730 |

| Tesla Motors, Inc., NASDAQ | TSLA | 318.82 | -0.75(-0.23%) | 25803 |

| The Coca-Cola Co | KO | 44.81 | 0.08(0.18%) | 4222 |

| Twitter, Inc., NYSE | TWTR | 19.85 | -0.09(-0.45%) | 33231 |

| UnitedHealth Group Inc | UNH | 186.75 | 0.40(0.21%) | 10299 |

| Verizon Communications Inc | VZ | 43.75 | 0.09(0.21%) | 919 |

| Visa | V | 97 | 0.17(0.18%) | 13641 |

| Wal-Mart Stores Inc | WMT | 76.35 | -0.02(-0.03%) | 747 |

| Walt Disney Co | DIS | 104.7 | -0.09(-0.09%) | 902 |

| Yandex N.V., NASDAQ | YNDX | 31.47 | 0.13(0.41%) | 3011 |

NIKE (NKE) initiated with a Hold at Needham

UnitedHealth (UNH) target raised to $235 from $200 at Mizuho

Facebook (FB) target raised to $185 from $165 at Needham

Goldman Sachs (GS) downgraded to Mkt Perform from Outperform at Keefe Bruyette

Boeing (BA) upgraded to Neutral from Underperform at BofA/Merrill

Manufacturing sales increased for the third consecutive month, up 1.1% to $54.6 billion in May. The gain was mainly attributable to higher sales in the transportation equipment and chemical manufacturing industries.

Sales were up in 16 of 21 industries, representing 71% of the manufacturing sector. Sales of durable goods rose 2.2%, while sales of non-durable goods declined 0.3%.

In constant dollars, sales were up 1.1%, indicating that higher volumes of manufactured goods were sold in May.

Sales in the transportation equipment industry rose 4.2% to $11.5 billion in May, the third gain in four months. The growth was the result of increases in the motor vehicle (+8.6%) and the motor vehicle parts (+5.7%) industries, mainly reflecting higher volumes. After removing the effect of price changes, sales in volume terms rose 8.1% and 5.0% respectively in these industries in May.

Privately-owned housing units authorized by building permits in June were at a seasonally adjusted annual rate of 1,254,000. This is 7.4 percent above the revised May rate of 1,168,000 and is 5.1 percent above the June 2016 rate of 1,193,000. Single-family authorizations in June were at a rate of 811,000; this is 4.1 percent above the revised May figure of 779,000. Authorizations of units in buildings with five units or more were at a rate of 409,000 in June.

Privately-owned housing starts in June were at a seasonally adjusted annual rate of 1,215,000. This is 8.3 percent above the revised May estimate of 1,122,000 and is 2.1 percent above the June 2016 rate of 1,190,000. Single-family housing starts in June were at a rate of 849,000; this is 6.3 percent above the revised May figure of 799,000. The June rate for units in buildings with five units or more was 359,000.

Morgan Stanley (MS) reported Q2 FY 2017 earnings of $0.87 per share (versus $0.75 in Q2 FY 2016), beating analysts' consensus estimate of $0.77.

The company's quarterly revenues amounted to $9.503 bln (+6.7% y/y), beating analysts' consensus estimate of $9.052 bln.

MS rose to $46.10 (+2.13%) in pre-market trading.

IBM (IBM) reported Q2 FY 2017 earnings of $2.97 per share (versus $2.95 in Q2 FY 2016), beating analysts' consensus estimate of $2.74.

The company's quarterly revenues amounted to $19.289 bln (-4.7% y/y), generally in-line with analysts' consensus estimate of $19.452 bln.

The company also reaffirmed guidance for FY 2017, projecting EPS of 'at least' $13.80 versus analysts' consensus estimate of $13.68.

IBM fell to $149.50 (-2.92%) in pre-market trading.

-

Gets 1 tick price tail at 2023 gilt sale

-

Gets 0.2 basis point yield tail at 2023 gilt sale

-

Britain's new business council will be attended by business leaders representing a range of sectors, particularly those likely to be most affected by Brexit - May's spokesman

EUR/USD

Resistance levels (open interest**, contracts)

$1.1636 (5255)

$1.1614 (1545)

$1.1601 (748)

Price at time of writing this review: $1.1538

Support levels (open interest**, contracts):

$1.1495 (452)

$1.1462 (873)

$1.1425 (1896)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date August, 4 is 67597 contracts (according to data from July, 18) with the maximum number of contracts with strike price $1,1500 (5255);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3177 (3030)

$1.3152 (2233)

$1.3106 (1699)

Price at time of writing this review: $1.3033

Support levels (open interest**, contracts):

$1.2973 (361)

$1.2942 (378)

$1.2908 (1040)

Comments:

- Overall open interest on the CALL options with the expiration date August, 4 is 27362 contracts, with the maximum number of contracts with strike price $1,3100 (3030);

- Overall open interest on the PUT options with the expiration date August, 4 is 25151 contracts, with the maximum number of contracts with strike price $1,2800 (2957);

- The ratio of PUT/CALL was 0.92 versus 0.93 from the previous trading day according to data from July, 18

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

Equity markets lacked direction in Asia on Wednesday, as was the case overnight in the U.S., though Australian stocks outperformed on strong gains among the country's biggest banks. Markets are expected to remain in narrow ranges ahead of policy statements from the European and Japanese central banks, due Thursday. Some investors are avoiding aggressive trading as a result.

Stocks across Europe dropped on Tuesday, with the exporter-heavy DAX 30 index DAX, -1.25% ending 1.3% lower at 12,430.39-its worst session since June 29. More broadly, European benchmarks finished the session under pressure as the euro stepped up to a 14-month high against the U.S. dollar and as disappointing corporate earnings reports rolled in. A stronger euro can hurt European exporters as it makes products more expensive for overseas customers.

The S&P 500 and the Nasdaq closed at records on Tuesday as gains in tech stocks offset weakness in telecom services and energy shares. A surge in Netflix Inc. NFLX, +13.54% shares on the back of strong earnings gave the broader tech sector a boost and helped to underpin the large-cap index push into the positive territory.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers