- Analytics

- News and Tools

- Market News

CFD Markets News and Forecasts — 18-01-2018

(raw materials / closing price /% change)

Oil 63.72 -0.39%

Gold 1,327.00 -0.91%

(index / closing price / change items /% change)

Nikkei -104.97 23763.37 -0.44%

TOPIX -13.96 1876.86 -0.74%

Hang Seng +138.53 32121.94 +0.43%

CSI 300 +23.30 4271.42 +0.55%

Euro Stoxx 50 +8.13 3620.91 +0.23%

FTSE 100 -24.47 7700.96 -0.32%

DAX +97.47 13281.43 +0.74%

CAC 40 +0.84 5494.83 +0.02%

DJIA -97.84 26017.81 -0.37%

S&P 500 -4.53 2798.03 -0.16%

NASDAQ -2.23 7296.05 -0.03%

S&P/TSX -42.24 16284.46 -0.26%

(pare/closed(GMT +3)/change, %)

EUR/USD $1,2238 +0,45%

GBP/USD $1,3893 +0,47%

USD/CHF Chf0,95891 -0,66%

USD/JPY Y111,10 -0,18%

EUR/JPY Y135,97 +0,27%

GBP/JPY Y154,343 +0,30%

AUD/USD $0,7998 +0,35%

NZD/USD $0,7300 +0,41%

USD/CAD C$1,24157 -0,14%

07:00 Germany Producer Price Index (YoY) December 2.5% 2.3%

07:00 Germany Producer Price Index (MoM) December 0.1% 0.2%

08:15 Switzerland Producer & Import Prices, y/y December 1.8%

09:00 Eurozone Current account, unadjusted, bln November 35.9

09:30 United Kingdom Retail Sales (MoM) December 1.1% 0.3%

09:30 United Kingdom Retail Sales (YoY) December 1.6% 2.1%

13:30 Canada Foreign Securities Purchases November 20.81

13:30 Canada Manufacturing Shipments (MoM) November -0.4% 2%

15:00 U.S. Reuters/Michigan Consumer Sentiment Index (Preliminary) January 95.9 97

17:15 U.S. FOMC Member Quarles Speaks

18:00 U.S. Baker Hughes Oil Rig Count January 752

Major stock markets in the US recorded a slight decline, as the fall in the shares of the utilities sector and basic resources halted the rally, which had previously led to the Dow Jones index's maximum increase of 1000 points.

Investors also acted out ambiguous data for the United States. The US Department of Commerce said that the growth rate of housing construction in the US weakened more than expected in December, recording the biggest recession slightly more than a year, amid a sharp decline in the construction of single-family housing units after a two-month growth. The laying of new homes fell 8.2% to a seasonally adjusted level of 1.192 million units. The November sales were revised to 1,299 million units from previously announced 1,297 million units. The December percentage decline was the largest since November 2016. Economists predicted that the bookmarks will drop to 1.275 million units. The construction permit decreased by 0.1% to 1.302 million units in December. Construction permits increased by 4.7% to 1.263 million units in 2017, which is also the highest level since 2007.

Meanwhile, the Ministry of Labor reported that the number of Americans applying for unemployment benefits fell more than expected last week, to the lowest level in 45 years, but the decline was likely to overstate the health of the labor market, as the data in the several states. Initial applications for state unemployment benefits fell by 41,000 to 220,000, seasonally adjusted for the week ending January 13, the lowest level since February 1973. The appeals for the previous week were not revised. Economists predicted that bids would fall to 250,000.

Most components of the DOW index finished trading in positive territory (16 out of 30). The leader of growth was UnitedHealth Group Incorporated (UNH, + 2.07%). Outsider were shares of General Electric Company (GE, -3.00%).

Most S & P sectors recorded a decline. The largest drop was shown by the utilities sector (-0.7%). The technological sector grew most (+ 0.2%).

At closing:

DJIA -0.37% 26.017.81 -97.84

Nasdaq -0.03% 7.296.05 -2.23

S & P -0.16% 2,798.03 -4.53

U.S. commercial crude oil inventories (excluding those in the Strategic Petroleum Reserve) decreased by 6.9 million barrels from the previous week. At 412.7 million barrels, U.S. crude oil inventories are in the middle of the average range for this time of year.

Total motor gasoline inventories increased by 3.6 million barrels last week, and are in the middle of the average range. Both finished gasoline inventories and blending components inventories increased last week. Distillate fuel inventories decreased by 3.9 million barrels last week and are in the lower half of the average range for this time of year. Propane/propylene inventories decreased by 3.7 million barrels last week, and are in the lower half of the average range. Total commercial petroleum inventories decreased by 13.8 million barrels last week.

Nikkei 225 on 4-hour time frame chart we can see that the price is forming an upside trend line.

Therefore, we can consider two scenarios either to enter short or long, the breakout or the bounce of this trend line.

U.S. stock-index futures fell slightly on Thursday, as investors were cautious after Wall Street rocketed to new records the day before. The focus was on quarterly results of Morgan Stanley (MS) as well as a batch of economic data.

Global Stocks:

Nikkei 23,763.37 -104.97 -0.44%

Hang Seng 32,121.94 +138.53 +0.43%

Shanghai 3,475.91 +31.24 +0.91%

S&P/ASX 6,014.60 -1.20 -0.02%

FTSE 7,695.57 -29.86 -0.39%

CAC 5,490.02 -3.97 -0.07%

DAX 13,241.16 +57.20 +0.43%

Crude $63.78 (-0.30%)

Gold $1,330.40 (-0.66%)

(company / ticker / price / change ($/%) / volume)

| ALCOA INC. | AA | 52.23 | -4.76(-8.35%) | 225869 |

| ALTRIA GROUP INC. | MO | 70.2 | 0.05(0.07%) | 509 |

| Amazon.com Inc., NASDAQ | AMZN | 1,293.80 | -1.20(-0.09%) | 23160 |

| American Express Co | AXP | 100.9 | 0.14(0.14%) | 7071 |

| AMERICAN INTERNATIONAL GROUP | AIG | 61.5 | 0.08(0.13%) | 353 |

| Apple Inc. | AAPL | 178.92 | -0.18(-0.10%) | 197689 |

| AT&T Inc | T | 36.87 | 0.02(0.05%) | 11097 |

| Barrick Gold Corporation, NYSE | ABX | 14.7 | 0.08(0.55%) | 25287 |

| Boeing Co | BA | 351.45 | 0.44(0.13%) | 38693 |

| Caterpillar Inc | CAT | 169 | 0.50(0.30%) | 6616 |

| Chevron Corp | CVX | 133 | 0.64(0.48%) | 497 |

| Cisco Systems Inc | CSCO | 41.11 | -0.09(-0.22%) | 9439 |

| Citigroup Inc., NYSE | C | 77.85 | 0.38(0.49%) | 14055 |

| Exxon Mobil Corp | XOM | 88.28 | 0.28(0.32%) | 789 |

| Ford Motor Co. | F | 12.25 | 0.07(0.57%) | 84520 |

| Freeport-McMoRan Copper & Gold Inc., NYSE | FCX | 19.78 | 0.01(0.05%) | 4763 |

| General Electric Co | GE | 17.39 | 0.04(0.23%) | 1113160 |

| General Motors Company, NYSE | GM | 44 | -0.03(-0.07%) | 2235 |

| Goldman Sachs | GS | 254 | 0.35(0.14%) | 4037 |

| Google Inc. | GOOG | 1,133.37 | 1.39(0.12%) | 1241 |

| Hewlett-Packard Co. | HPQ | 23.6 | 0.14(0.60%) | 310 |

| Home Depot Inc | HD | 200 | 0.18(0.09%) | 1045 |

| Intel Corp | INTC | 44.38 | -0.01(-0.02%) | 30700 |

| International Business Machines Co... | IBM | 170.22 | 1.57(0.93%) | 51070 |

| JPMorgan Chase and Co | JPM | 113.15 | 0.16(0.14%) | 14523 |

| Merck & Co Inc | MRK | 61.79 | -0.24(-0.39%) | 1865 |

| Microsoft Corp | MSFT | 90.1 | -0.04(-0.04%) | 16838 |

| Procter & Gamble Co | PG | 90.45 | -0.06(-0.07%) | 2745 |

| Starbucks Corporation, NASDAQ | SBUX | 61.25 | 0.59(0.97%) | 27558 |

| Tesla Motors, Inc., NASDAQ | TSLA | 346.5 | -0.66(-0.19%) | 6582 |

| Twitter, Inc., NYSE | TWTR | 24.59 | 0.03(0.12%) | 41109 |

| United Technologies Corp | UTX | 134.75 | 0.33(0.25%) | 629 |

| UnitedHealth Group Inc | UNH | 239.4 | 0.97(0.41%) | 4263 |

| Verizon Communications Inc | VZ | 51.9 | 0.18(0.35%) | 2213 |

| Visa | V | 122 | 0.02(0.02%) | 2758 |

| Wal-Mart Stores Inc | WMT | 104.75 | 2.05(2.00%) | 49594 |

Caterpillar (CAT) initiated with a Buy at Berenberg; target $200

Freeport-McMoRan (FCX) target raised to $18 from $16 at B. Riley FBR

Chevron (CVX) downgraded to Hold from Buy at HSBC Securities

The broadest measures of current conditions remained positive this month, although indexes for general activity, new orders, and employment declined from their readings in December. The firms reported higher prices for both inputs and their own manufactured goods this month. The future indexes reflecting expected growth over the next six months remained at high levels, although the indexes fell from their readings in December.

The index for current manufacturing activity in the region decreased from a revised reading of 27.9 in December to 22.2 this month.

Privately-owned housing units authorized by building permits in December were at a seasonally adjusted annual rate of 1,302,000. This is 0.1 percent below the revised November rate of 1,303,000, but is 2.8 percent above the December 2016 rate of 1,266,000. Single-family authorizations in December were at a rate of 881,000; this is 1.8 percent above the revised November figure of 865,000. Authorizations of units in buildings with five units or more were at a rate of 382,000 in December. An estimated 1,263,400 housing units were authorized by building permits in 2017. This is 4.7 percent (±0.6%) above the 2016 figure of 1,206,600.

Privately-owned housing starts in December were at a seasonally adjusted annual rate of 1,192,000. This is 8.2 percent below the revised November estimate of 1,299,000 and is 6.0 percent below the December 2016 rate of 1,268,000. Single-family housing starts in December were at a rate of 836,000; this is 11.8 percent below the revised November figure of 948,000. The December rate for units in buildings with five units or more was 352,000. An estimated 1,202,100 housing units were started in 2017. This is 2.4 percent above the 2016 figure of 1,173,800.

In the week ending January 13, the advance figure for seasonally adjusted initial claims was 220,000, a decrease of 41,000 from the previous week's unrevised level of 261,000. This is the lowest level for initial claims since February 24, 1973 when it was 218,000. The 4-week moving average was 244,500, a decrease of 6,250 from the previous week's unrevised average of 250,750.

Morgan Stanley (MS) reported Q4 FY 2017 earnings of $0.84 per share (versus $0.81 in Q4 FY 2016), beating analysts' consensus estimate of $0.78. (! Q4 results excluded a net discrete tax provision of $0.990 bln or a loss of $0.55 per share).

The company's quarterly revenues amounted to $9.500 bln (+5.3% y/y), beating analysts' consensus estimate of $9.249 bln.

MS rose to $56.25 (+1.63%) in pre-market trading.

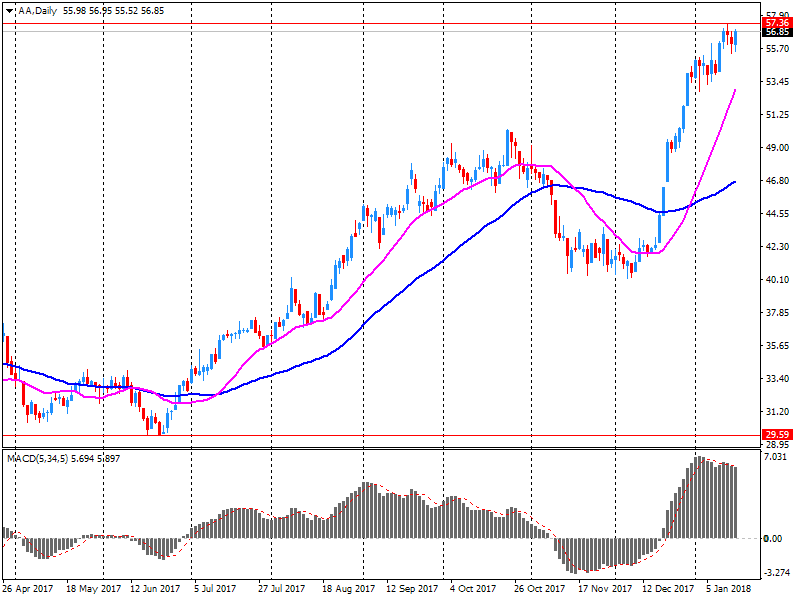

Alcoa (AA) reported Q4 FY 2017 earnings of $1.04 per share (versus $0.14 in Q4 FY 2016), missing analysts' consensus estimate of $1.23.

The company's quarterly revenues amounted to $3.174 bln (+25.1% y/y), missing analysts' consensus estimate of $3.285 bln.

AA fell to $53.20 (-6.65%) in pre-market trading.

EUR/USD: 1.2000 (2.4 b), 1.2100-05 (781 m), 1.2180 (553 m), 1.2200 (549 m), 1.2220(767 m), 1.2300 (627 m)

USD/JPY: 110.80 (1.5 b), 111.00-05 (1.5 b), 112.50 (701 m)

USD/CAD: 1.2400 (570 m), 1.2460 (780 m)

NZD/USD: 0.7025 (2.0 b)

EUR/GBP: 0.8650 (860 m), 0.8765 (862 m)

EUR/USD

Resistance levels (open interest**, contracts)

$1.2340 (4044)

$1.2310 (5514)

$1.2287 (3098)

Price at time of writing this review: $1.2188

Support levels (open interest**, contracts):

$1.2144 (1506)

$1.2111 (1757)

$1.2073 (2246)

Comments:

- Overall open interest on the CALL options and PUT options with the expiration date February, 9 is 106667 contracts (according to data from January, 17) with the maximum number of contracts with strike price $1,2100 (5514);

GBP/USD

Resistance levels (open interest**, contracts)

$1.3944 (3177)

$1.3928 (3482)

$1.3909 (897)

Price at time of writing this review: $1.3817

Support levels (open interest**, contracts):

$1.3735 (228)

$1.3700 (508)

$1.3663 (208)

Comments:

- Overall open interest on the CALL options with the expiration date February, 9 is 33837 contracts, with the maximum number of contracts with strike price $1,3600 (3482);

- Overall open interest on the PUT options with the expiration date February, 9 is 28546 contracts, with the maximum number of contracts with strike price $1,3500 (3055);

- The ratio of PUT/CALL was 0.84 versus 0.86 from the previous trading day according to data from January, 17

* - The Chicago Mercantile Exchange bulletin (CME) is used for the calculation.

** - Open interest takes into account the total number of option contracts that are open at the moment.

China's economy expanded at a steady pace at the end of 2017, data from the National Bureau of Statistics showed, cited by rttnews.

Gross domestic product climbed 6.8 percent year-on-year in the fourth quarter, the same pace of growth as seen in the third quarter. The rate was forecast to slow to 6.7 percent.

In 2017, the economy expanded at a faster pace of 6.9 percent after rising 6.7 percent in 2016, and exceeded the government's 2017 target of about 6.5 percent.

Another report showed that industrial production advanced 6.2 percent annually, slightly faster than the 6.1 percent increase seen in November. The rate was forecast to remain unchanged at 6.1 percent.

For the whole year of 2017, industrial production grew 6.6 percent, as expected.

Trend estimates (monthly change)

-

Employment increased 25,000 to 12,419,800.

-

Unemployment increased 100 to 715,000.

-

Unemployment rate decreased by less than 0.1 pts to 5.4%.

-

Participation rate remained steady at 65.5%.

-

Monthly hours worked in all jobs increased 4.0 million hours (0.2%) to 1,738.4 million hours.

Seasonally adjusted estimates (monthly change)

-

Employment increased 34,700 to 12,440,800. Full-time employment increased 15,100 to 8,518,900 and part-time employment increased 19,500 to 3,921,800.

-

Unemployment increased 20,500 to 730,600. The number of unemployed persons looking for full-time work increased 9,900 to 501,800 and the number of unemployed persons only looking for part-time work increased 10,600 to 228,800.

-

Unemployment rate increased 0.1 pts to 5.5%

-

Participation rate increased by 0.2 pts to 65.7%.

-

Monthly hours worked in all jobs decreased 4.2 million hours (0.2%) to 1,736.4 million hours.

European stocks finished in the red Wednesday, as a round of corporate financial updates failed to lift an investing mood dimmed by losses on U.S. stock markets. A disappointing sales report from fashion house Burberry Group PLC and a warning of layoffs at Swedish construction company Skanska AB dragged on shares of those companies.

The Dow industrials on Wednesday staged a late rally to end above 26,000 for the first time ever, knocking out another round-number milestone at a history-setting pace for blue chips, with all the main equity indexes finishing at all-time highs. An upbeat gauge of conditions at the Federal Reserve's business districts contributed to the buying sentiment.

Asia-Pacific stocks were higher Thursday, aided by strength in Chinese banks and regional tech companies, after equities hit fresh record highs on Wall Street overnight. Hong Kong stocks HSI, +0.12% were 0.4% higher and benchmarks on the mainland logged similar gains. Bank stocks in China rose after data showed housing prices rose last month in 57 of 70 cities measured by the National Bureau of Statistics.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers