- Analytics

- News and Tools

- Market News

Market Trading News and Research from 25 April 2024

Here is what you need to know on Thursday, April 25:

The US Dollar (USD) stays under modest selling pressure on Thursday as investors gear up for key data releases. The US Bureau of Economic Analysis will publish the first estimate of the annualized Gross Domestic Product (GDP) growth for the first quarter and the Department of Labor will release the weekly Initial Jobless Claims data.

Following Tuesday's sharp decline, the USD Index registered small losses on Wednesday, supported by the upbeat Durable Goods Orders data for March. Additionally, the cautious market stance further helped the currency stay resilient against its risk-sensitive rivals. Early Thursday, the USD Index stays in negative territory and edges lower toward 105.50. The US economy is forecast to grow at an annual rate of 2.5% in Q1, following the 3.4% expansion recorded in the last quarter of 2023. Meanwhile, US stock index futures stretch lower in the European morning and the 10-year US yield continues to fluctuate above 4.6%.

EUR/USD gained traction and climbed to its highest level in nearly two weeks above 1.0720 after closing virtually unchanged on Monday. Several European Central Bank (ECB) policymakers will be delivering speeches throughout the day.

US Dollar price this week

The table below shows the percentage change of US Dollar (USD) against listed major currencies this week. US Dollar was the weakest against the Australian Dollar.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.60% | -1.02% | -0.44% | -1.47% | 0.66% | -0.91% | 0.22% | |

| EUR | 0.59% | -0.41% | 0.16% | -0.86% | 1.25% | -0.30% | 0.81% | |

| GBP | 0.99% | 0.39% | 0.58% | -0.46% | 1.67% | 0.11% | 1.22% | |

| CAD | 0.43% | -0.16% | -0.56% | -1.03% | 1.09% | -0.47% | 0.66% | |

| AUD | 1.45% | 0.86% | 0.45% | 1.02% | 2.09% | 0.55% | 1.66% | |

| JPY | -0.66% | -1.26% | -1.68% | -1.10% | -2.14% | -1.57% | -0.44% | |

| NZD | 0.89% | 0.30% | -0.13% | 0.46% | -0.56% | 1.54% | 1.11% | |

| CHF | -0.20% | -0.83% | -1.24% | -0.64% | -1.67% | 0.46% | -1.10% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

GBP/USD closed the second consecutive day in positive territory on Wednesday and continued to push higher in the early European session on Thursday. The pair was last seen trading within a few pips of 1.2500.

USD/JPY broke above 155.00 and reached its highest level in several decades above 155.50. The Bank of Japan (BoJ) will announce monetary policy decisions during the Asian trading hours on Friday.

Japanese Yen struggles near multi-decade low ahead of US GDP; looks to BoJ on Friday.

Gold (XAU/USD) closed with marginal losses on Wednesday. After edging lower toward $2,300 in the Asian session on Thursday, XAU/USD staged a rebound and was last seen trading above $2,320.

Gold price remains confined in a range, $2,300 holds the key for bulls ahead of US GDP.

Economic Indicator

Gross Domestic Product Annualized

The real Gross Domestic Product (GDP) Annualized, released quarterly by the US Bureau of Economic Analysis, measures the value of the final goods and services produced in the United States in a given period of time. Changes in GDP are the most popular indicator of the nation’s overall economic health. The data is expressed at an annualized rate, which means that the rate has been adjusted to reflect the amount GDP would have changed over a year’s time, had it continued to grow at that specific rate. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Last release: Thu Mar 28, 2024 12:30

Frequency: Quarterly

Actual: 3.4%

Consensus: 3.2%

Previous: 3.2%

Source: US Bureau of Economic Analysis

The US Bureau of Economic Analysis (BEA) releases the Gross Domestic Product (GDP) growth on an annualized basis for each quarter. After publishing the first estimate, the BEA revises the data two more times, with the third release representing the final reading. Usually, the first estimate is the main market mover and a positive surprise is seen as a USD-positive development while a disappointing print is likely to weigh on the greenback. Market participants usually dismiss the second and third releases as they are generally not significant enough to meaningfully alter the growth picture.

- The United States Gross Domestic Product is seen expanding at an annualized rate of 2.5% in Q1.

- The current resilience of the US economy bolsters the case for a soft landing.

- Markets now see the US Federal Reserve starting its easing cycle in September.

The US Bureau of Economic Analysis (BEA) will publish the first estimate of the US Gross Domestic Product (GDP) for the January-March period on Thursday. The report is expected to show an economic expansion of 2.5% after growing at an annualized pace of 3.4% during the prior quarter.

Forecasting US Gross Domestic Product: Deciphering the Numbers

Thursday's economic agenda in the US features the unveiling of the initial GDP report for the first quarter, set to be disclosed at 12:30 GMT. Analysts anticipate that the first assessment will reveal a 2.5% growth rate for the world's largest economy in the January–March period, a moderately robust pace, albeit markedly slower than the 3.4% expansion recorded in the preceding quarter.

From the latest release of the BEA: “Real GDP increased 2.5 percent in 2023 (from the 2022 annual level to the 2023 annual level), compared with an increase of 1.9 percent in 2022. The increase in real GDP in 2023 primarily reflected increases in consumer spending, nonresidential fixed investment, state and local government spending, exports, and federal government spending that were partly offset by decreases in residential fixed investment and private inventory investment. Imports decreased”.

Market participants will also pay close attention to the GDP Price Index (GDP Deflator), which represents the average change in prices of all new, domestically produced final goods and services in an economy over a specific period, typically a year or a quarter. It essentially reflects the inflation or deflation rate within an economy. During the last quarter of 2023, the GDP Price Index rose by 1.7% and is now seen rising by 3.0%.

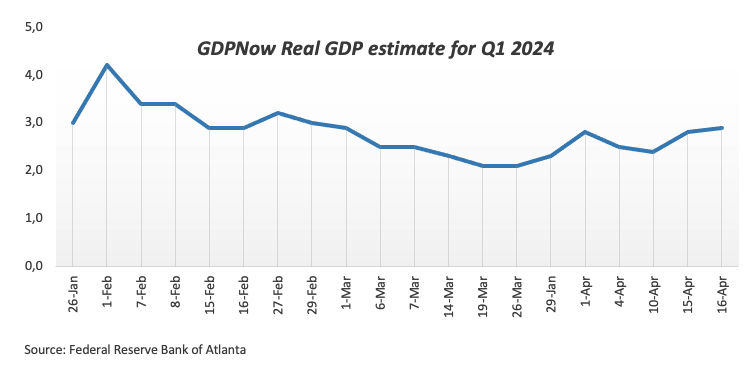

Furthermore, the Atlanta Fed GDPNow real GDP estimate for Q1 also props up the case for a solid performance of the US economy during that period.

According to analysts at TD Securities: “GDP growth likely modestly cooled to start the year, but to a still firm pace following two stronger expansions at 4.9% and 3.4% q/q annualized rate (AR) in Q3 and Q4 of last year, respectively. Growth in final domestic sales was likely firmer in 24Q1 than the headline would suggest (TD: 2.8% q/q AR), as we look for net trade & inventories to modestly dent still solid consumer spending.”

When is the GDP print released, and how can it affect the USD?

The US GDP report will be published at 12:30 GMT on Thursday. Meanwhile, the Greenback seems to have embarked on a consolidative phase ahead of the first estimate of US Q1 GDP as well as the inflation tracked by the Personal Consumption Expenditures Price Index (PCE) due on Friday.

Meanwhile, the macroeconomic outlook remains consistent with growing anticipation among market participants of the US Federal Reserve's (Fed) first interest rate reduction in September. On this, CME Group’s FedWatch Tool sees the probability of a lower interest rate at around 70%, up from nearly 3% a month ago.

Still around the commencement of the Fed’s easing cycle, Atlanta Federal Reserve Bank President Raphael Bostic predicted US inflation would reach 2% more gradually than previously predicted but did not rush to cut rates. New York Federal Reserve Bank President John Williams emphasized that the Fed's decisions are based on positive data and the strength of the economy, adding that the Fed may adjust if higher rates are needed. Fed Governor Michelle Bowman suggests that efforts to reduce inflation may have hit a snag, leaving uncertainty about interest rates' ability to return to the bank's target. Finally, in his latest comments, Fed Chairman Jerome Powell showed no rush to start reducing interest rates, matching the broad-based rate setters’ views.

A sneak peek ahead of the results

Stronger-than-anticipated GDP growth in the first quarter could bolster expectations that the Fed will delay the start of its easing programme, probably until September or December, which should in turn morph into further strength in the US Dollar (USD). The Greenback is also expected to hold its ground in the case of a higher GDP Price Deflator.

Alternatively, an abrupt change of heart around the US Dollar and, hence, a challenge to the current markets’ bets for a rate cut later in the year, should require an unexpectedly worse-than-estimated print, which appears quite unlikely for the time being.

Techs on the US Dollar Index (DXY)

Pablo Piovano, Senior Analyst at FXStreet, notes: “In case the bullish sentiment gathers steam, the USD Index (DXY) could confront the so-far 2024 top at 106.51 (April 16). Surpassing this level could encourage market participants to embark on a potential visit to the November peak at 107.11 (November 1), just ahead of the 2023 high at 107.34 (October 3).”

Pablo adds: “If we look in the opposite direction, the April bottom at 103.88 (April 9) remains underpinned by the 200-day Simple Moving Average (SMA) at 103.99, and this area is expected to offer decent contention. The breakdown of this region exposes a drop to the 100-day SMA at 103.67 prior to the March low at 102.35 (March 8).”

Economic Indicator

Gross Domestic Product Annualized

The real Gross Domestic Product (GDP) Annualized, released quarterly by the US Bureau of Economic Analysis, measures the value of the final goods and services produced in the United States in a given period of time. Changes in GDP are the most popular indicator of the nation’s overall economic health. The data is expressed at an annualized rate, which means that the rate has been adjusted to reflect the amount GDP would have changed over a year’s time, had it continued to grow at that specific rate. Generally speaking, a high reading is seen as bullish for the US Dollar (USD), while a low reading is seen as bearish.

Read more.Next release: Thu Apr 25, 2024 12:30 (Prel)

Frequency: Quarterly

Consensus: 2.5%

Previous: 3.4%

Source: US Bureau of Economic Analysis

The US Bureau of Economic Analysis (BEA) releases the Gross Domestic Product (GDP) growth on an annualized basis for each quarter. After publishing the first estimate, the BEA revises the data two more times, with the third release representing the final reading. Usually, the first estimate is the main market mover and a positive surprise is seen as a USD-positive development while a disappointing print is likely to weigh on the greenback. Market participants usually dismiss the second and third releases as they are generally not significant enough to meaningfully alter the growth picture.

GDP FAQs

A country’s Gross Domestic Product (GDP) measures the rate of growth of its economy over a given period of time, usually a quarter. The most reliable figures are those that compare GDP to the previous quarter e.g Q2 of 2023 vs Q1 of 2023, or to the same period in the previous year, e.g Q2 of 2023 vs Q2 of 2022. Annualized quarterly GDP figures extrapolate the growth rate of the quarter as if it were constant for the rest of the year. These can be misleading, however, if temporary shocks impact growth in one quarter but are unlikely to last all year – such as happened in the first quarter of 2020 at the outbreak of the covid pandemic, when growth plummeted.

A higher GDP result is generally positive for a nation’s currency as it reflects a growing economy, which is more likely to produce goods and services that can be exported, as well as attracting higher foreign investment. By the same token, when GDP falls it is usually negative for the currency. When an economy grows people tend to spend more, which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation with the side effect of attracting more capital inflows from global investors, thus helping the local currency appreciate.

When an economy grows and GDP is rising, people tend to spend more which leads to inflation. The country’s central bank then has to put up interest rates to combat the inflation. Higher interest rates are negative for Gold because they increase the opportunity-cost of holding Gold versus placing the money in a cash deposit account. Therefore, a higher GDP growth rate is usually a bearish factor for Gold price.

- EUR/JPY gains traction near 166.85 on Thursday, the highest level since 2008.

- The cross keeps the bullish vibe, with the overbought RSI condition.

- The first resistance level will emerge at 166.82; the initial support level is located at 165.35.

The EUR/JPY cross trades in positive territory for the fifth consecutive day during the early European trading hours on Thursday. The cross edges higher to 166.85, its highest level since 2008. The Tokyo April Consumer Price Index (CPI) will be due on Friday ahead of the Bank of Japan (BoJ) interest rate decision. The markets expect the Japanese central bank to leave its policy rate and bond purchase amounts unchanged since BoJ raised interest rates in March for the first time since 2007. The divergence in rates between Japan and the Eurozone is the key factor that weighs the Japanese Yen (JPY) against the Euro (EUR).

Technically, EUR/JPY maintains the bullish stance unchanged on the four-hour chart as the cross is above the 50-period and 100-period Exponential Moving Averages (EMA) with an upward slope. The Relative Strength Index (RSI) holds in bullish territory above 70. However, the overbought RSI condition indicates that further consolidation cannot be ruled out before positioning for any near-term EUR/JPY appreciation.

The first upside barrier for the cross will emerge near the upper boundary of the Bollinger Band at 166.82. The next hurdle is seen at the 167.00 psychological level. A bullish breakout above this level will see a rally to a yearly high of 2007 at 168.95, en route to an all-time high of 169.78 in July 2008.

On the flip side, the initial support level for the cross is located near a high of March 20 at 165.35. Further south, the next contention level to watch is the 50-period EMA at 165.11, followed by the 100-period EMA at 164.62. A breach of this level will see a drop to the lower limit of the Bollinger Band at 164.30.

EUR/JPY four-hour chart

FX option expiries for Apr 25 NY cut at 10:00 Eastern Time, via DTCC, can be found below

- EUR/USD: EUR amounts

- 1.0595 390m

- 1.0640 1.2b

- 1.0650 990m

- 1.0700 750m

- 1.0750 767m

- 1.0760 642m

- 1.0800 689m

- 1.0850 839m

- GBP/USD: GBP amounts

- 1.2410 400m

- 1.2500 432m

- USD/JPY: USD amounts

- 153.00 1.7b

- 154.00 1.2b

- 155.00 1.9b

- 155.25 441m

- 155.85 1.2b

- AUD/USD: AUD amounts

- 0.6430 559m

- 0.6635 505m

- USD/CAD: USD amounts

- 1.3650 379m

- 1.3750 457m

- EUR/USD could approach the 21-day EMA at 1.0727.

- A break below 1.0700 could lead the pair toward the major support of 1.0650 and April’s low at 1.0601.

- A breach above the major level of 1.0695 suggests a weakening of bearish sentiment.

EUR/USD recovers its recent losses registered in the previous session, trading around 1.0710 during the Asian session on Thursday. From a technical standpoint, analysis suggests a weakening of bearish sentiment for the pair as it has surpassed the major level of 1.0695 and the psychological level of 1.0700.

Additionally, the lagging indicator Moving Average Convergence Divergence (MACD) indicates a shift in momentum for the EUR/USD pair, as it is positioned below the centerline but above the signal line. However, the 14-day Relative Strength Index (RSI) remains below the 50-mark, indicating a continuation of bearish momentum.

Key support for the EUR/USD pair is likely to be found around the psychological level of 1.0700. A breach below this level could apply downward pressure on the pair, potentially leading it toward the region surrounding the major support level of 1.0650. Further support may be identified around April’s low at 1.0601, which aligns with the psychological level of 1.0600.

On the upside, the immediate barrier for the pair could be the 21-day Exponential Moving Average (EMA) at 1.0727. A breakthrough above this level could propel the pair towards the 38.2% Fibonacci retracement level at 1.0749, which is drawn between the levels of 1.0981 and 1.0606, coinciding with the major level of 1.0750.

EUR/USD: Daily Chart

- USD/CHF drifts lower to 0.9145 on the softer US Dollar on Thursday.

- The hawkish tone of the US Fed has lifted the USD, creating a tailwind for the pair.

- Switzerland’s ZEW Survey Expectations rose to 17.6 in April, compared to 11.5 prior.

The USD/CHF pair trades on a weaker note near 0.9145 during the early European session on Thursday. Traders seem to prefer to wait on the sidelines ahead of the release of the US preliminary Gross Domestic Product (GDP) Annualized for the first quarter (Q1) later in the day. In the meantime, any development surrounding escalating tensions in the Middle East might boost safe-haven assets like the Swiss Franc (CHF).

The US Federal Reserve's (Fed) policymakers agreed with the central bank’s position to remain on hold. The hawkish tone of the Fed has provided some support to the Greenback in recent weeks. However, investors have doubts about exactly when monetary policy easing will come. The US GDP growth number might offer some hints about how the US economy performs in Q1 of 2024.

The first estimated US GDP growth number is estimated to grow at a 2.5% annualized pace during the first quarter, compared to the previous reading of 3.4%. In case the report shows stronger-than-expected data, this might trigger speculation that the US Fed will delay the rate cut cycle, which might lift the US Dollar (USD).

On Wednesday, data released from the Centre for European Economic Research showed that Switzerland’s ZEW Survey Expectations improved to 17.6 in April compared to 11.5 in the previous reading. Apart from this, the ongoing geopolitical tensions in the Middle East might lift the CHF, a traditional safe-haven currency, and drag the USD/CHF lower.

- NZD/USD gains momentum as investors express optimism regarding the de-escalation of tensions between Israel and Iran.

- The higher US Treasury yields could help in limiting the losses of the US Dollar.

- US GDP Annualized (Q1) is expected to grow at a slower rate in the first quarter.

The NZD/USD pair moves in the positive direction, trading around 0.5940 during the Asian session on Thursday. The risk-sensitive New Zealand Dollar (NZD) gains momentum as risk appetite improves. Investors are optimistic about the resolution of conflicts between Iran and Israel, following a statement by an Iranian official suggesting no immediate plans for retaliation against Israeli airstrikes, as reported by Reuters.

The China Securities Journal reported on Tuesday that the People's Bank of China (PBoC) plans to reduce the Medium-term Lending Facility (MLF) rate to decrease funding costs during the next MLF rate setting scheduled for May 15. Lower MLF rates in China could stimulate economic activity and boost consumer spending, which may lead to increased demand for New Zealand goods and services in the Chinese market.

The US Dollar Index (DXY), which measures the US Dollar (USD) against six major currencies, depreciated following mixed manufacturing data from the United States (US). However, the Greenback's losses were somewhat offset by slight gains in US Treasury yields.

According to the US Department of Commerce's report on Wednesday, US Durable Goods Orders rose 2.6% month-over-month (MoM) in March, surpassing the previous reading of 0.7% and beating the estimated 2.5%. However, core goods, excluding transportation, increased 0.2% MoM, falling short of the expected 0.3%.

On Thursday, the preliminary Gross Domestic Product Annualized (Q1) data for the United States (US) is set to be released, with expectations of a growth rate slowdown. These GDP figures will offer insights into the strength of the US economy and could influence future actions by the Federal Reserve (Fed).

- GBP/USD struggles to attract follow-through buying and trades in a narrow range on Thursday.

- Reduced Fed rate cut bets and speculations about more aggressive BoE easing act as a headwind.

- The technical setup warrants some caution before positioning for any further appreciating move.

The GBP/USD pair consolidates its strong recovery gains registered over the past two days, from the 1.2300 mark or the YTD low set earlier this week and oscillates in a range during the Asian session on Thursday. Spot prices currently trade near the 1.2465 region, unchanged for the day as traders await more cues about the Federal Reserve's (Fed) rate-cut path before placing fresh directional bets.

Hence, the focus will remain glued to important US macro data – the Advance Q1 GDP report later today and the Personal Consumption Expenditures (PCE) Price Index on Friday. In the meantime, expectations that the Fed will delay cutting interest rates in the wake of sticky inflation continue to act as a tailwind for the US Dollar (USD). Apart from this, speculations about more aggressive policy easing by the Bank of England (BoE) undermine demand for the British Pound (GBP) and act as a headwind for the GBP/USD pair.

From a technical perspective, acceptance above the 23.6% Fibonacci retracement level of the March-April downfall favors bullish traders and supports prospects for a further appreciating move. Hence, some follow-through strength beyond the 1.2500 psychological mark, en route to the 1.2530-1.2535 region or the 38.2% Fibo. level, looks like a distinct possibility. That said, oscillators on the daily chart are still holding in the negative territory, suggesting that the latter should act as a headwind and cap the upside for the GBP/USD pair.

On the flip side, the 1.2425 area now seems to protect the immediate downside ahead of the 1.2400 round figure. Some follow-through selling could drag the GBP/USD pair back towards the 1.2350 intermediate support en route to the 1.2300 mark, or the YTD low touched on Tuesday. A convincing break below the latter will be seen as a fresh trigger for bearish traders and pave the way for an extension of the recent downtrend from the March swing high. Spot prices might then slide to the 1.2245 area before dropping to the 1.2200 mark.

GBP/USD daily chart

- Gold price remains confined in a narrow band for the second straight day on Thursday.

- Reduced Fed rate cut bets and a positive risk tone cap the upside for the commodity.

- Traders now await key US macro data before positioning for the near-term trajectory.

Gold price (XAU/USD) extends its consolidative price move above the $2,300 mark during the Asian session on Thursday as traders more cues about the Federal Reserve's (Fed) rate-cut path before placing fresh directional bets. Hence, the focus will remain glued to key US macro data – the Advance Q1 GDP report due later today and the Personal Consumption Expenditures (PCE) Price Index on Friday. This will play a key role in influencing the near-term US Dollar (USD) price dynamics and provide some meaningful impetus to the commodity.

In the meantime, the recent hawkish remarks by several Fed officials suggested that the central bank is in no rush to cut interest rates.

Moreover, stronger US consumer inflation figures forced investors to scale back their expectations about the timing of the first rate cut to September and downsize the number of rate cuts in 2024. This keeps the US Treasury bond yields elevated and acts as a headwind for the non-yielding Gold price. Apart from this, easing concerns about a major escalation of the Middle East crisis continues to cap the safe-haven XAU/USD.

Daily Digest Market Movers: Gold price struggles to gain traction amid hawkish Fed expectations

- Investors await key US economic data for clarity about the timing when the Federal Reserve will start cutting rates, leading to subdued range-bound price action around the Gold price for the second straight day on Thursday.

- The first estimate, or the Advance US GDP report is due for release later today and is expected to show that the world's largest economy grew by 2.5% annualized pace during the first quarter as compared to the 3.4% previous.

- The focus will then shift to the Fed's preferred inflation gauge – the core Personal Consumption Expenditures (PCE) Price Index – on Friday, which will play a key role in determining the near-term trajectory for the XAU/USD.

- The US Census Bureau reported on Wednesday that Durable Goods Orders climbed 2.6% in March as compared to the previous month's downwardly revised 0.7% increase, while new orders excluding transportation rose 0.2%.

- This comes on the back of strong US consumer inflation figures and hawkish remarks by Fed officials, reaffirming bets that the central bank will not begin its rate-cutting cycle before September and capping the non-yielding metal.

- The global risk sentiment remains supported by easing concerns about a further escalation of geopolitical tensions in the Middle East, which is seen as another factor acting as a headwind for the safe-haven precious metal.

- The US Dollar bulls seem reluctant to place aggressive bets and remain on the defensive ahead of important macro releases, offering some support to the XAU/USD and limiting any meaningful downside for now.

Technical Analysis: Gold price bears need to wait for acceptance below $2,300 before placing fresh bets

From a technical perspective, the Gold price now seems to have found acceptance below the 23.6% Fibonacci retracement level of the February-April rally, albeit showing some resilience below the $2,300 mark earlier this week. Moreover, oscillators on the daily chart – though have been losing traction – are still holding in the positive territory. Hence, it will be prudent to wait for some follow-through selling below the $2,300-2,290 area, or over a two-week low touched on Tuesday, before positioning for an extension of the recent pullback from the all-time peak. The subsequent downfall has the potential to drag the XAU/USD to the $2,260-2,255 area, or the 38.2% Fibo. level, en route to the $2,225 intermediate support and the $2,200-2,190 confluence, comprising the 50% Fibo. level and the 50-day Simple Moving Average (SMA).

On the flip side, immediate resistance is pegged near the $2,325 area ahead of the overnight swing high, the $2,337-2,338 zone. A sustained move beyond could allow the Gold price to test the next relevant hurdle near the $2,350-2,355 region and climb further towards the $2,380 supply zone. This is closely followed by the $2,400 round figure and the all-time peak, near the $2,431-2,432 area, which if cleared will set the stage for an extension of the recent blowout rally witnessed over the past two months or so.

Gold FAQs

Gold has played a key role in human’s history as it has been widely used as a store of value and medium of exchange. Currently, apart from its shine and usage for jewelry, the precious metal is widely seen as a safe-haven asset, meaning that it is considered a good investment during turbulent times. Gold is also widely seen as a hedge against inflation and against depreciating currencies as it doesn’t rely on any specific issuer or government.

Central banks are the biggest Gold holders. In their aim to support their currencies in turbulent times, central banks tend to diversify their reserves and buy Gold to improve the perceived strength of the economy and the currency. High Gold reserves can be a source of trust for a country’s solvency. Central banks added 1,136 tonnes of Gold worth around $70 billion to their reserves in 2022, according to data from the World Gold Council. This is the highest yearly purchase since records began. Central banks from emerging economies such as China, India and Turkey are quickly increasing their Gold reserves.

Gold has an inverse correlation with the US Dollar and US Treasuries, which are both major reserve and safe-haven assets. When the Dollar depreciates, Gold tends to rise, enabling investors and central banks to diversify their assets in turbulent times. Gold is also inversely correlated with risk assets. A rally in the stock market tends to weaken Gold price, while sell-offs in riskier markets tend to favor the precious metal.

The price can move due to a wide range of factors. Geopolitical instability or fears of a deep recession can quickly make Gold price escalate due to its safe-haven status. As a yield-less asset, Gold tends to rise with lower interest rates, while higher cost of money usually weighs down on the yellow metal. Still, most moves depend on how the US Dollar (USD) behaves as the asset is priced in dollars (XAU/USD). A strong Dollar tends to keep the price of Gold controlled, whereas a weaker Dollar is likely to push Gold prices up.

- The Australian Dollar gains ground as the stronger CPI enhances hawkish sentiment regarding the RBA monetary policy stance.

- The Australian Dollar strengthens in response to the higher 10-year yield on Australian government bonds.

- The gains in US Treasury yields could limit the losses of the US Dollar.

The Australian Dollar (AUD) edges higher for the fourth consecutive session on Thursday. The Australian Dollar (AUD) gained traction against the US Dollar (USD) following the release of robust Australian Consumer Price Index (CPI) figures on Wednesday. Additionally, the easing tensions in the Middle East have created a positive market sentiment, favoring risk-sensitive currencies like the AUD and consequently supporting the AUD/USD pair.

The Australian Dollar gains ground following the higher 10-year yield on Australian government bonds, which has surged above 4.49%, approaching five-month highs. This increase in yield is attributed to the growing expectations of a more hawkish stance from the Reserve Bank of Australia (RBA) regarding its interest rate trajectory.

The US Dollar Index (DXY), which gauges the US Dollar (USD) against six major currencies, downticks, possibly influenced by improved risk appetite. However, the modest gains in US Treasury yields could mitigate the losses of the Greenback.

The preliminary Gross Domestic Product Annualized (Q1) from the United States (US) is scheduled to be released on Thursday, with expectations of a slowdown in the growth rate. The GDP figures will provide insights into the strength of the US economy and may indicate the Federal Reserve (Fed)'s future actions. If the report reveals higher-than-expected figures, it could spark speculation that the Fed will postpone its rate cut cycle.

Daily Digest Market Movers: Australian Dollar appreciates after hotter CPI data

- Luci Ellis, the chief economist at Westpac and former Assistant Governor (Economic) at the Reserve Bank of Australia, notes that inflation slightly exceeded expectations in the March quarter. Westpac anticipates that the Board will keep interest rates unchanged in May and has adjusted their forecasted date for the first rate cut from September to November this year.

- Australia’s Consumer Price Index (CPI) rose by 1.0% QoQ in the first quarter of 2024, against the expected 0.8% and 0.6% prior. CPI (YoY) increased by 3.6% compared to the forecast of 3.4% for Q1 and 4.1% prior.

- Australia’s Monthly Consumer Price Index (YoY) rose to 3.5% in March, against the market expectations and the previous reading of 3.4%.

- The S&P Global US Composite PMI decreased in April, indicating only a modest expansion in the nation's private sector. This was the weakest expansion since December. Activity saw slower growth rates in both the manufacturing and service sectors, with expansions easing to three- and five-month lows, respectively.

- In April 2024, the Judo Bank Australia Composite Output Index rose, marking the third consecutive month of expansion in the Australian private sector and the fastest pace since April 2022. Although the service sector primarily drove business activity growth, the rate of decline in manufacturing output slowed to its lowest level in eight months.

- The China Securities Journal indicated on Tuesday that the People's Bank of China (PBoC) plans to reduce the Medium-term Lending Facility (MLF) rate in an effort to decrease funding costs. The next MLF rate setting is scheduled for May 15. This move might potentially benefit Australian exports to China, considering the strong trade ties between the two nations.

Technical Analysis: Australian Dollar hovers above the psychological level of 0.6500

The Australian Dollar trades around 0.6510 on Thursday. The pair is hovering above the lower boundary of a symmetrical triangle pattern. A further gain could lead to a bullish sentiment, with the pair potentially targeting the psychological level of 0.6600 and aiming for the upper boundary of the triangle near 0.6639. Additionally, the 14-day Relative Strength Index (RSI) is above the 50-level, supporting this bullish outlook.

On the downside, immediate support is expected around the psychological level of 0.6500. A break below this level may lead to further downside momentum, with the next significant support region around 0.6456. The AUD/USD pair may find further support at April’s low of 0.6362.

AUD/USD: Daily Chart

Australian Dollar price today

The table below shows the percentage change of the Australian Dollar (AUD) against listed major currencies today. The Australian Dollar was the strongest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.05% | -0.03% | -0.04% | -0.04% | 0.14% | -0.01% | 0.02% | |

| EUR | 0.05% | 0.05% | 0.01% | 0.00% | 0.18% | 0.03% | 0.07% | |

| GBP | 0.02% | -0.04% | -0.04% | -0.04% | 0.16% | -0.02% | 0.03% | |

| CAD | 0.06% | 0.00% | 0.05% | 0.01% | 0.19% | 0.04% | 0.07% | |

| AUD | 0.04% | 0.00% | 0.03% | 0.00% | 0.18% | 0.02% | 0.07% | |

| JPY | -0.13% | -0.19% | -0.15% | -0.19% | -0.16% | -0.16% | -0.12% | |

| NZD | 0.03% | -0.03% | 0.00% | -0.04% | -0.03% | 0.16% | 0.08% | |

| CHF | -0.02% | -0.07% | -0.04% | -0.07% | -0.07% | 0.12% | -0.05% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate, and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- Indian Rupee trades with mild negative bias on Thursday.

- The INR’s downside might be capped, owing to a further decline in crude oil prices.

- Market players will closely monitor the US preliminary GDP growth number for the first quarter (Q1).

Indian Rupee (INR) extends its downside on Thursday despite the decline of the US Dollar (USD). The growing speculation that the US Federal Reserve (Fed) will delay interest rate cuts boosts the Greenback against its rivals. Nonetheless, the upside of the pair might be limited due to a further decline in crude oil prices amid easing tensions about a wider fallout between Iran and Israel.

Investors will closely monitor the US preliminary Gross Domestic Product (GDP) Annualized for the first quarter (Q1). The report could offer a clue of how strongly the US economy is growing and point to the Fed's next move. On Friday, the final reading of the US March Personal Consumption Expenditures Price Index (PCE) will be a closely watched event. Apart from this, India’s general election, which started on 19 April and will run until 1 June, will be in the spotlight.

Daily Digest Market Movers: The Indian Rupee remains vulnerable at the start of the election

- In mid-April, India’s foreign exchange reserves stood at USD 564.5 billion (+48 billion over a year), equating to more than 7.6 months of goods and services imports.

- The Indian rupee remains stable at the start of the election period, holding up better than other Asian currencies so far. Since the start of April, it has only depreciated by 0.6% against the US Dollar.

- The Indian economy needs to grow at a rate of 8–10% per annum over the next decade to reap the demographic dividend, according to the Reserve Bank of India (RBI) monthly bulletin.

- The main economic challenge for the Indian government after the election is unemployment, according to economists polled by Reuters, who forecast India to expand at a solid 6.5% this fiscal year.

- The US Durable Goods Orders improved 2.6% MoM or $7.3 billion, to $283.4 billion in March, compared to the 0.7% increase (revised from 1.4%) in February. The increase in overall orders was the biggest since November 2023

- Durable Goods Orders ex Transportation rose by 0.2% MoM in March, while new orders excluding defense rose 2.3% MoM in the same period. Both figures came in below the consensus.

Technical analysis: USD/INR keeps the bullish vibe in the longer term

The Indian Rupee trades on a softer note on the day. USD/INR maintains the positive outlook unchanged on the daily timeframe as the pair is above the key 100-day Exponential Moving Average (EMA). Nonetheless, the 14-day Relative Strength Index (RSI) hovers around the 50.00 midlines, suggesting that further consolidation is favorable for the time being.

The first upside barrier for USD/INR will emerge at 83.50 (high of April 15). Any follow-through buying above this level will expose 83.72 (an all-time high), en route to 84.00 (round figure). On the other hand, the confluence of the 100-day EMA and a low of April 10 near the 83.10–83.15 zone. The additional downside filter to watch is 82.78 (low of January 15), followed by 82.65 (low of March 16).

US Dollar price today

The table below shows the percentage change of US Dollar (USD) against listed major currencies today. US Dollar was the strongest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.06% | -0.06% | -0.06% | -0.13% | 0.11% | -0.12% | -0.01% | |

| EUR | 0.06% | -0.01% | 0.00% | -0.07% | 0.17% | -0.07% | 0.03% | |

| GBP | 0.07% | -0.02% | 0.01% | -0.08% | 0.17% | -0.07% | 0.02% | |

| CAD | 0.08% | 0.00% | 0.00% | -0.06% | 0.16% | -0.04% | 0.05% | |

| AUD | 0.13% | 0.05% | 0.07% | 0.05% | 0.21% | 0.00% | 0.12% | |

| JPY | -0.11% | -0.16% | -0.17% | -0.18% | -0.23% | -0.25% | -0.12% | |

| NZD | 0.11% | 0.04% | 0.06% | 0.02% | -0.02% | 0.21% | 0.13% | |

| CHF | 0.01% | -0.04% | -0.06% | -0.06% | -0.11% | 0.12% | -0.09% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Indian Rupee FAQs

The Indian Rupee (INR) is one of the most sensitive currencies to external factors. The price of Crude Oil (the country is highly dependent on imported Oil), the value of the US Dollar – most trade is conducted in USD – and the level of foreign investment, are all influential. Direct intervention by the Reserve Bank of India (RBI) in FX markets to keep the exchange rate stable, as well as the level of interest rates set by the RBI, are further major influencing factors on the Rupee.

The Reserve Bank of India (RBI) actively intervenes in forex markets to maintain a stable exchange rate, to help facilitate trade. In addition, the RBI tries to maintain the inflation rate at its 4% target by adjusting interest rates. Higher interest rates usually strengthen the Rupee. This is due to the role of the ‘carry trade’ in which investors borrow in countries with lower interest rates so as to place their money in countries’ offering relatively higher interest rates and profit from the difference.

Macroeconomic factors that influence the value of the Rupee include inflation, interest rates, the economic growth rate (GDP), the balance of trade, and inflows from foreign investment. A higher growth rate can lead to more overseas investment, pushing up demand for the Rupee. A less negative balance of trade will eventually lead to a stronger Rupee. Higher interest rates, especially real rates (interest rates less inflation) are also positive for the Rupee. A risk-on environment can lead to greater inflows of Foreign Direct and Indirect Investment (FDI and FII), which also benefit the Rupee.

Higher inflation, particularly, if it is comparatively higher than India’s peers, is generally negative for the currency as it reflects devaluation through oversupply. Inflation also increases the cost of exports, leading to more Rupees being sold to purchase foreign imports, which is Rupee-negative. At the same time, higher inflation usually leads to the Reserve Bank of India (RBI) raising interest rates and this can be positive for the Rupee, due to increased demand from international investors. The opposite effect is true of lower inflation.

| Raw materials | Closed | Change, % |

|---|---|---|

| Silver | 27.142 | -0.47 |

| Gold | 2315.15 | -0.3 |

| Palladium | 998.86 | -1.57 |

- The Japanese Yen continues losing ground amid the divergent BoJ-Fed policy expectations.

- The recent intervention warnings by Japanese authorities do little to provide any respite.

- Traders now look to the US Q1 GDP report for some impetus ahead of the BoJ on Friday.

The Japanese Yen (JPY) extends its weakening trend further below the 155.00 psychological mark and drops to the lowest level since June 1990 against its American counterpart during the Asian session on Thursday. The wide interest-rate differential between Japan and the United States (US) is seen as a key factor that continues to undermine the JPY. The move, however, fuels the risk of a potential intervention by Japanese authorities, which, in turn, might hold back the JPY bears from placing fresh bets. Traders might also prefer to move to the sidelines ahead of the crucial Bank of Japan (BoJ) monetary policy decision on Friday.

The Japanese central bank is widely expected to leave policy settings, and bond purchase amounts unchanged after raising interest rates in March for the first time since 2007. In contrast, investors seem convinced that the Federal Reserve (Fed) may delay cutting interest rates in the wake of still sticky inflation, which remains supportive of elevated US Treasury bond yields and acts as a tailwind for the US Dollar (USD). This, in turn, suggests that the path of least resistance for the USD/JPY pair remains to the upside.

Daily Digest Market Movers: Japanese Yen bears not ready to give up despite intervention warnings

Expectations that the difference in interest rates between the US and Japan will stay wide drag the Japanese Yen to a fresh multi-decade low on Thursday, fueling speculation about possible intervention by Japanese authorities.

Japanese officials have repeatedly warned that they will take necessary action to address excessive moves in the yen if needed and have emphasized a focus on the pace of the currency’s depreciation rather than a precise price level.

Moreover, Bank of Japan Governor Kazuo Ueda has said the central bank may hike rates again if the fall in the domestic currency significantly pushes up inflation, which might hold back the JPY bears from placing fresh bets.

Japan's Liberal Democratic Party (LDP) executive, Takao Ochi, said on Wednesday that the JPY's fall towards the 160 against its American counterpart may be deemed excessive and could prompt policymakers to consider some action.

Japan's Finance Minister Shunichi Suzuki refrained from commenting on specific FX levels, while Chief Cabinet Secretary Yoshimasa Hayashi reiterated that it is important for currencies to move in a stable manner reflecting fundamentals.

Investors keenly await the outcome of the highly-anticipated two-day BoJ policy meeting on Friday for cues on when the central bank will raise interest rates again, which, in turn, will determine the near-term trajectory for the JPY.

The US Census Bureau reported on Wednesday that Durable Goods Orders increased by 2.6% in March as compared to the previous month's downwardly revised 0.7% rise, while new orders excluding transportation rose 0.2%

This comes on the back of strong US consumer inflation figures and reaffirmed expectations that the Federal Reserve will not begin its rate-cutting cycle before September, which acts as a tailwind for the US Dollar and the USD/JPY pair.

Traders now look forward to the release of the Advance US GDP report, which is expected to show that growth in the world's largest economy slowed to a 2.5% annualized pace during the first quarter of 2024 from the 3.4% previous.

Apart from this, the US Personal Consumption Expenditures (PCE) Price Index on Friday will be looked upon for cues about the Fed's rate-cut path and determining the next leg of a directional move for the buck and the currency pair.

Technical Analysis: USD/JPY could consolidate before the next leg up towards the 156.00 mark

From a technical perspective, the overnight breakout through a short-term trading range and a subsequent strength beyond the 155.00 mark could be seen as a fresh trigger for bullish traders. That said, the Relative Strength Index (RSI) on the daily chart remains in the overbought territory, warranting some caution amid intervention fears and ahead of the BoJ event risk. Hence, it will be prudent to wait for some near-term consolidation or a modest pullback before positioning for the next leg of a positive move. Nevertheless, the USD/JPY pair seems poised to prolong its recent well-established uptrend from the March swing low and aim to conquer the 156.00 round figure.

On the flip side, any meaningful corrective slide is likely to attract fresh buyers and remain limited near the 154.90-154.85 region. This is followed by the 154.55-154.45 support zone, which, if broken, might prompt some technical selling and drag the USD/JPY pair to the 154.00 round-figure mark. The downward trajectory could extend further towards last Friday's low, around the 153.60-153.55 area.

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The current BoJ ultra-loose monetary policy, based on massive stimulus to the economy, has caused the Yen to depreciate against its main currency peers. This process has exacerbated more recently due to an increasing policy divergence between the Bank of Japan and other main central banks, which have opted to increase interest rates sharply to fight decades-high levels of inflation.

The BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supports a widening of the differential between the 10-year US and Japanese bonds, which favors the US Dollar against the Japanese Yen.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

Japan’s Chief Cabinet Secretary Yishimasa Hayashi said on Thursday that he “won't comment on forex levels or forex intervention” but he “will be ready to take full response.”

Additional comments

Important for currencies to move in stable manner reflecting fundamentals.

Rapid FX moves undesirable.

Closely watching FX moves.

Expect the Bank of Japan (BoJ) to work closely with govternment.

Expect BoJ to conduct appropriate monetary policy to sustainably, stably hit its price target, working closely with govt.

Market reaction

USD/JPY is testing multi-decade highs near 155.50 despite the Japanese verbal intervention, up 0.04% on the day.

Japanese Yen FAQs

The Japanese Yen (JPY) is one of the world’s most traded currencies. Its value is broadly determined by the performance of the Japanese economy, but more specifically by the Bank of Japan’s policy, the differential between Japanese and US bond yields, or risk sentiment among traders, among other factors.

One of the Bank of Japan’s mandates is currency control, so its moves are key for the Yen. The BoJ has directly intervened in currency markets sometimes, generally to lower the value of the Yen, although it refrains from doing it often due to political concerns of its main trading partners. The current BoJ ultra-loose monetary policy, based on massive stimulus to the economy, has caused the Yen to depreciate against its main currency peers. This process has exacerbated more recently due to an increasing policy divergence between the Bank of Japan and other main central banks, which have opted to increase interest rates sharply to fight decades-high levels of inflation.

The BoJ’s stance of sticking to ultra-loose monetary policy has led to a widening policy divergence with other central banks, particularly with the US Federal Reserve. This supports a widening of the differential between the 10-year US and Japanese bonds, which favors the US Dollar against the Japanese Yen.

The Japanese Yen is often seen as a safe-haven investment. This means that in times of market stress, investors are more likely to put their money in the Japanese currency due to its supposed reliability and stability. Turbulent times are likely to strengthen the Yen’s value against other currencies seen as more risky to invest in.

- AUD/JPY continues its winning streak after the stronger Australian CPI was released on Wednesday.

- Australia’s 10-year government bond yield has surged to 4.49% near five-month highs on waning expectations of the RBA rate cuts.

- The Japanese Yen continues to depreciate as the BoJ is expected to abstain from implementing rate hikes on Friday.

AUD/JPY edges higher for the fourth consecutive session on Thursday. The Australian Dollar (AUD) found support following the release of Australian Consumer Price Index (CPI) data on Wednesday, which exceeded expectations. This development hints at a potentially hawkish stance for the Reserve Bank of Australia’s (RBA) monetary policy, bolstering the AUD and subsequently supporting the AUD/JPY pair.

Australia’s 10-year government bond yield has surged above 4.49%, nearing five-month highs, as robust domestic inflation figures have strengthened expectations of the RBA delaying interest rate cuts. Moreover, easing tensions in the Middle East has fostered a positive market sentiment, benefiting risk-sensitive currencies like the AUD.

The Japanese Yen (JPY) continues to depreciate ahead of the upcoming release of the Bank of Japan’s (BoJ) Monetary Policy Statement scheduled for Friday. It's widely anticipated that the BoJ will abstain from implementing rate hikes in this meeting.

According to reports from Nikkei, the BoJ is likely to deliberate on the "impact of accelerating Yen depreciation," indicating that the central bank may intervene in the foreign exchange markets if the JPY weakens.

Daily Digest Market Movers: AUD/JPY appreciates on hawkish sentiment surrounding RBA

- According to Luci Ellis, Westpac's chief economist and former Assistant Governor (Economic) at the Reserve Bank of Australia, inflation slightly surpassed expectations in the March quarter. They anticipate the Board will maintain interest rates in May and have revised the projected date for the initial rate reduction from September to November this year.

- Australia’s Consumer Price Index (CPI) rose by 1.0% QoQ in the first quarter of 2024, against the expected 0.8% and 0.6% prior. CPI (YoY) increased by 3.6% compared to the forecasted 3.4% for Q1 and 4.1% prior.

- Australia’s Monthly Consumer Price Index (YoY) rose by 3.5% in March, against the market expectations and the previous reading of 3.4%.

- On Tuesday, Australia's Judo Bank Composite Purchasing Managers Index (PMI) surged to a 24-month high, indicating an improvement from the previous month. While the Manufacturing PMI reached an eight-month high, the Services PMI declined to a two-month low. This has bolstered the hawkish sentiment for the RBA’s stance on its interest rate trajectory.

- According to the Japan Times, the proportion of Japanese companies intending to increase their pay scales reached 70.7%, marking a rise of 6.3 percentage points from the previous year. Additionally, the number of companies planning to implement pay-scale hikes and regular pay increases totaling 5% or more amounted to 36.5%, nearly doubling from the previous year. This could provide support for the Yen.

- Reuters reported that Bank of Japan (BoJ) Governor Kazuo Ueda reiterated on Tuesday that the central bank would raise interest rates again if trend inflation accelerates toward its 2% target, in line with its forecast. Ueda also said that it is hard to predict in advance the ideal timeframe for the Bank of Japan (BoJ) to gather sufficient data before considering a policy change.

- The Tokyo Consumer Price Index (CPI) for the year ended April is scheduled to be released during the early Friday session in Japan.

Technical Analysis: AUD/JPY moves above the psychological level of 101.00

The AUD/JPY trades around 101.10 on Thursday, edging towards the upper boundary of the daily ascending channel after surpassing April’s high of 100.81. Moreover, the 14-day Relative Strength Index (RSI) is trending above the 50-level, indicating a bullish sentiment. The immediate resistance is seen at the major level of 101.50.

In case of a downside movement, immediate support for the AUD/JPY pair could be found at the psychological level of 101.00, followed by the major support level of 100.81. A breach below this level might lead to a further decline toward the support level of 99.65, followed by the lower boundary of the ascending channel around the level of 99.00.

AUD/JPY: Daily Chart

Australian Dollar price this week

The table below shows the percentage change of the Australian Dollar (AUD) against listed major currencies this week. The Australian Dollar was the strongest against the Japanese Yen.

| USD | EUR | GBP | CAD | AUD | JPY | NZD | CHF | |

| USD | -0.46% | -0.71% | -0.29% | -1.22% | 0.49% | -0.70% | 0.35% | |

| EUR | 0.46% | -0.24% | 0.17% | -0.74% | 0.94% | -0.22% | 0.80% | |

| GBP | 0.70% | 0.24% | 0.40% | -0.50% | 1.18% | 0.01% | 1.05% | |

| CAD | 0.29% | -0.17% | -0.40% | -0.92% | 0.78% | -0.41% | 0.64% | |

| AUD | 1.20% | 0.75% | 0.50% | 0.91% | 1.68% | 0.51% | 1.55% | |

| JPY | -0.49% | -0.95% | -1.20% | -0.77% | -1.70% | -1.19% | -0.14% | |

| NZD | 0.68% | 0.23% | -0.03% | 0.39% | -0.52% | 1.17% | 1.04% | |

| CHF | -0.35% | -0.81% | -1.06% | -0.64% | -1.56% | 0.14% | -1.04% |

The heat map shows percentage changes of major currencies against each other. The base currency is picked from the left column, while the quote currency is picked from the top row. For example, if you pick the Euro from the left column and move along the horizontal line to the Japanese Yen, the percentage change displayed in the box will represent EUR (base)/JPY (quote).

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

- WTI edges lower to $82.45 on Thursday as the fear of wider war in the Middle East eased.

- Higher bets that the US Fed will delay rate cuts support the Greenback.

- US commercial crude stockpiles last week fell by 6.368 million barrels, the largest drawdown since mid-January.

Western Texas Intermediate (WTI), the US crude oil benchmark, is trading around $82.45 on Thursday. The black gold edges lower as the fear over wider conflict in the Middle East fades. Additionally, the hawkish tone from the Federal Reserve (Fed) boosts the US dollar (USD) and caps the upside of black gold.

Perceived de-escalation between Iran and Israel, and the flow of oil from the Middle East, which has not been interrupted by conflict in the region, dragged the WTI prices lower in the last few sessions. However, any sign of rising tensions in the Middle East and stricter sanctions against Iran might cap the downside of the WTI price.

Furthermore, the growing speculation that the US Federal Reserve (Fed will delay the interest rate provides some support to the Greenback and acts as a headwind for the black gold price. It’s worth noting that a strong dollar makes oil more expensive for holders of other currencies. Several US Fed officials noted that rate cuts aren’t coming in the coming months as inflation remains stickier than expected.

On the other hand. The US commercial crude stockpiles for the week ending April 19 fell by 6.368 million barrels from the previous reading of 2.735 million barrels built. This reading registered the largest drawdown since mid-January, according to data from the Energy Information Administration.

The People’s Bank of China (PBoC) set the USD/CNY central rate for the trading session ahead on Thursday at 7.1058 as compared to the previous day's fix of 7.1048 and 7.2472 Reuters estimates.

- EUR/USD posts modest gains near 1.0700 on the weaker USD on Thursday.

- US Durable Goods Orders increased by 2.6% MoM in March vs. 0.7% prior; Core Goods rose by 0.2% MoM, worse than expected.

- The dovish stance of the ECB, which sticks to plans to cut interest rates this year, weighs on the Euro.

- Traders will monitor the release of US Q1 GDP growth number data.

The EUR/USD pair hovers around the 1.0700 psychological level on Thursday during the early Asian session. The modest uptick of the major pair is supported by the softer US Dollar (USD). Later in the day, Germany’s GfK Consumer Confidence Survey for April will be released. Additionally, the US preliminary Gross Domestic Product (GDP) growth number will be due.

The US Department of Commerce revealed on Wednesday that Durable Goods Orders in the United States increased 2.6% MoM in March from a 0.7% rise in the previous reading, beating the estimation of 2.5%. Core goods, which excluded transportation, rose by 0.2% MoM, missing the expectation of 0.3%.

The release of US GDP for the first quarter could offer clues of how strong the economy is growing and point to the Fed's next move. If the report shows stronger-than-expected data, this might trigger speculation that the Fed will delay the rate cut cycle and boost the Greenback. Markets have priced in nearly 70% odds that the US Federal Reserve (Fed) will cut its benchmark rate in September, according to the CME FedWatch tool,

Across the pond, the European Central Bank (ECB) policymakers stick to plans to cut interest rates this year, even though elevated US inflation might delay a pivot to looser policy by the Fed. The ECB President Christine Lagarde suggested that the central bank may cut its deposit rate from a record-high 4% in June, but has kept its options open for further action. The dovish stance of the ECB exerts some selling pressure on the Euro (EUR) and creates a headwind for the EUR/USD pair.

| Index | Change, points | Closed | Change, % |

|---|---|---|---|

| NIKKEI 225 | 907.92 | 38460.08 | 2.42 |

| Hang Seng | 372.34 | 17201.27 | 2.21 |

| KOSPI | 52.73 | 2675.75 | 2.01 |

| ASX 200 | -0.5 | 7683 | -0.01 |

| DAX | -48.95 | 18088.7 | -0.27 |

| CAC 40 | -13.92 | 8091.86 | -0.17 |

| Dow Jones | -42.77 | 38460.92 | -0.11 |

| S&P 500 | 1.08 | 5071.63 | 0.02 |

| NASDAQ Composite | 16.11 | 15712.75 | 0.1 |

| Pare | Closed | Change, % |

|---|---|---|

| AUDUSD | 0.64952 | 0.1 |

| EURJPY | 166.051 | 0.24 |

| EURUSD | 1.06963 | -0.06 |

| GBPJPY | 193.424 | 0.37 |

| GBPUSD | 1.24594 | 0.07 |

| NZDUSD | 0.5933 | -0.03 |

| USDCAD | 1.37026 | 0.29 |

| USDCHF | 0.91452 | 0.3 |

| USDJPY | 155.243 | 0.29 |

FOREIGN EXCHANGE MARKET NEWS

CURRENCY MARKET DEFINITION

The concept of currency market has several definitions:

- Currency market is the sphere of economic relations that are manifested in the purchase and sale of currency values (foreign currency, securities in foreign currency), as well as operations related to the investment of capital in foreign currency;

- Currency market is a financial center where currency purchase and sale transactions based on supply and demand for them are concentrated;

- Curency market is a whole of authorized banks, investment companies, brokerages, exchanges, and foreign banks that perform foreign exchange operations.

- Currency market is a whole of communications systems that link banks in different countries that conduct international currency transactions.

Simply put, currency market is the market where currency transactions are made, that is, the currency of one country is exchanged for the currency of another country at a certain exchange rate. The exchange rate is the relative price of currencies of two countries or the currency of one country expressed in another country's monetary units.

Currency market is part of the global financial market, where many operations related to the global movement of capital take place.

TYPES OF MARKETS. RUSSIAN AND INTERNATIONAL CURRENCY MARKETS

There are international and domestic currency markets.

Domestic currency market — is a market within a single country.

The international currency market — is a global market that covers currency markets of all countries in the world. It does not have a specific site where trading is carried out. All operations within it are carried out through a system of cable and satellite channels that link the world's regional currency markets. Regional markets today include the Asian (with centers in Tokyo, Hong Kong, Singapore, and Melbourne), the European (London, Frankfurt am Main, and Zurich), and the American (New York, Chicago, and Los Angeles) markets.

Currency trading on the international currency market is carried out on the basis of market exchange rates, which are set on the basis of supply and demand in the market and under the influence of various macroeconomic data. Forex is the international currency market.

Currency markets can also be divided into exchange and over-the-counter markets. Exchange currency market is an organized market where trading is carried out through an exchange—a special company that sets trading rules and provides all the conditions for organizing trading under these rules.

Over-the-counter currency market — is a market where there are no certain trading rules, and purchase and sale operations are not linked to a specific place of trade, as opposed to the case of an exchange.

As a rule, an over-the-counter currency market is organized by special companies that provide services for the purchase and sale of currencies, which may or may not be members of the currency exchange. Trading operations in this market are now carried out mainly via the Internet.

The over-the-counter currency market is much larger than the exchange market in terms of trading volume. The Forex international over-the-counter currency market is considered the most liquid in the world. It operates around the clock in all financial centers of the world (from New York to Tokyo).

CURRENCY MARKET FUNCTIONS

Currency market— is the most important platform for ensuring the normal course of all global economic processes.

The main macroeconomic functions of the currency market are:

- creating conditions for the subjects of foreign exchange relations to make timely international current and capital payments and thereby promoting the development of foreign trade;

- providing conditions and mechanisms for the implementation of monetary and economic policy of the state;

- diversifying foreign exchange reserves;

- forming the exchange rate under the influence of supply and demand;

NEWS IMPACT

Various currencies are the main trading tool in the currency market. Exchange rates are formed under the influence of supply and demand in the market.

In addition to that, currency rates are influenced by many fundamental factors related to the global economic situation, events in national economies, and political decisions.

News about these factors can be found in various sources:

- Reports showing a country´s level of economic development.

The more stable an economy is developing, the more stable its currency is. Accordingly, it is possible to predict how the currency will behave in the near future, based on statistical data published in official sources of countries with a certain regularity.

This data includes:

- GDP

- unemployment;

- return on equity;

- consumer price index;

- industrial price index;

- propensity to consume;

- salaries outside of the agricultural sector;

- residential construction, etc.

Interest rate level, set by national authorities regulating credit policy, is an equally important indicator. In the European Union, this is ECB–the European Central Bank, in the US, this is the Federal Reserve System, in Japan—the Bank of Japan, in the UK—the Bank of England, in Switzerland—the Swiss national Bank, etc.

The interest rate level is determined at meetings of the national central bank. Then, the decision on the rate is published in official sources. If the central bank of a country reduces the interest rate, the money supply in the country increases, and the national currency depreciates against other world currencies. If the interest rate increases, the national currency will strengthen.

- Speeches of country leaders, leading economists and analysts.

A speech or even a separate statement by a country's leader can reverse a trend. Speeches on these topics may change the currency exchange rate:

- analysis of the situation on the currency market;

- changes in monetary or economic policy;

- adoption of a budget policy;

- forecasts of the economic situation, etc.

All this news is published in various sources. Major international news is more or less easy to find in Russian, but news related to the domestic economic policy and the economy of foreign countries is much less common in the Russian press. Mostly, such news is published by the national media and in the language of the country where the news is published.

It is very difficult for one person to follow all the news at once, and they are likely to miss some important event that can turn the whole situation on the market upside down. Guided by our main principle—to create the best trading conditions for our customers—we try to select the most important news from all over the world and publish them on our website.

The TeleTRADE Department of Analytics monitors news on most national and international news sources on a daily basis and identifies those that can potentially affect exchange rates. These are the main news items that are included in our news feed.

In addition, all our clients have free access to the Dow Jones news feed. This is a joint project of Dow Jones Newswires, the world's largest news agency, and the leading Russian news agency Prime-TASS. The news feed is created specifically for currency traders and those who are interested in getting information about the world's currency markets.

© 2000-2024. All rights reserved.

This site is managed by Teletrade D.J. LLC 2351 LLC 2022 (Euro House, Richmond Hill Road, Kingstown, VC0100, St. Vincent and the Grenadines).

The information on this website is for informational purposes only and does not constitute any investment advice.

The company does not serve or provide services to customers who are residents of the US, Canada, Iran, The Democratic People's Republic of Korea, Yemen and FATF blacklisted countries.

Making transactions on financial markets with marginal financial instruments opens up wide possibilities and allows investors who are willing to take risks to earn high profits, carrying a potentially high risk of losses at the same time. Therefore you should responsibly approach the issue of choosing the appropriate investment strategy, taking the available resources into account, before starting trading.

Use of the information: full or partial use of materials from this website must always be referenced to TeleTrade as the source of information. Use of the materials on the Internet must be accompanied by a hyperlink to teletrade.org. Automatic import of materials and information from this website is prohibited.

Please contact our PR department if you have any questions or need assistance at pr@teletrade.global.

transfers